Market Data

January 19, 2018

China’s Economy Continues to See Robust Growth

Written by Tim Triplett

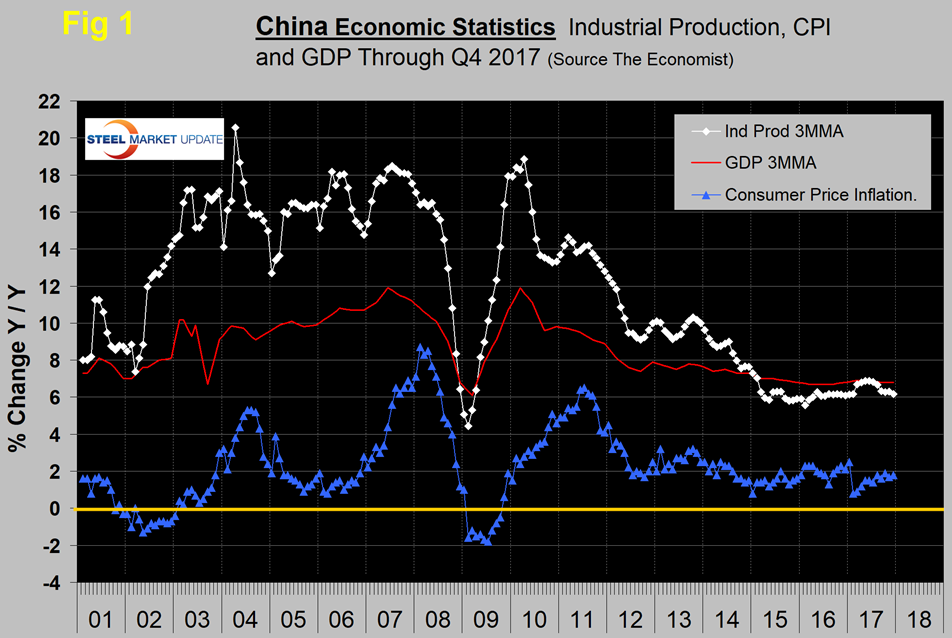

China’s steel production has continued to grow year over year, contradicting all the hoopla about production cuts, according to Steel Market Update’s latest analysis of Chinese government data. Once each quarter, we publish the official statistics for Chinese GDP, industrial production, consumer price inflation and fixed asset investment. Many analysts don’t believe these self-serving Party figures, but we include them in our reports because of the importance of China in the global steel scene. And these numbers are all that’s available. Figure 1 shows published data released this week for the growth of GDP, industrial production and consumer prices through the fourth quarter of 2017.

The GDP and industrial production portions of this graph are three-month moving averages. Wall Street Breakfast reported: “China’s economy grew at 6.9 percent in 2017 as a whole, the first growth acceleration in seven years and overshooting the government’s original full-year target of ‘around 6.5 percent.’ Despite the strong headline performance, many economists expect the slowdown to resume as a sustained campaign by Beijing to curb risky lending bites into investment in buildings, infrastructure and factory goods. GDP grew 6.8 percent year over year in the fourth quarter, the same result as in the third quarter. In the fourth quarter, exports of manufactured goods along with continued investment helped drive the economy.”

The three-month moving average (3MMA) of the growth of industrial production rose from 6.1 percent in January to 6.9 percent in June before falling back to 6.2 percent in December. Economy.com wrote: “Manufacturing remains the primary driver of China’s industrial production. Overall, production accelerated slightly to 6.2 percent year over year in December 2017, after it slowed to 6.1 percent in the month prior. Manufacturing sentiment remains buoyed thanks to a broad-based uptick in the global economy, which has increased external demand. However, domestic demand also improved in 2017 as evidenced by rising production of consumer durables such as automobiles. That said, bulk-commodity oriented industries remain a drag on production and are unlikely to rise in 2018. We expect the tailwind from global tech demand could slow in 2018 after a strong year.”

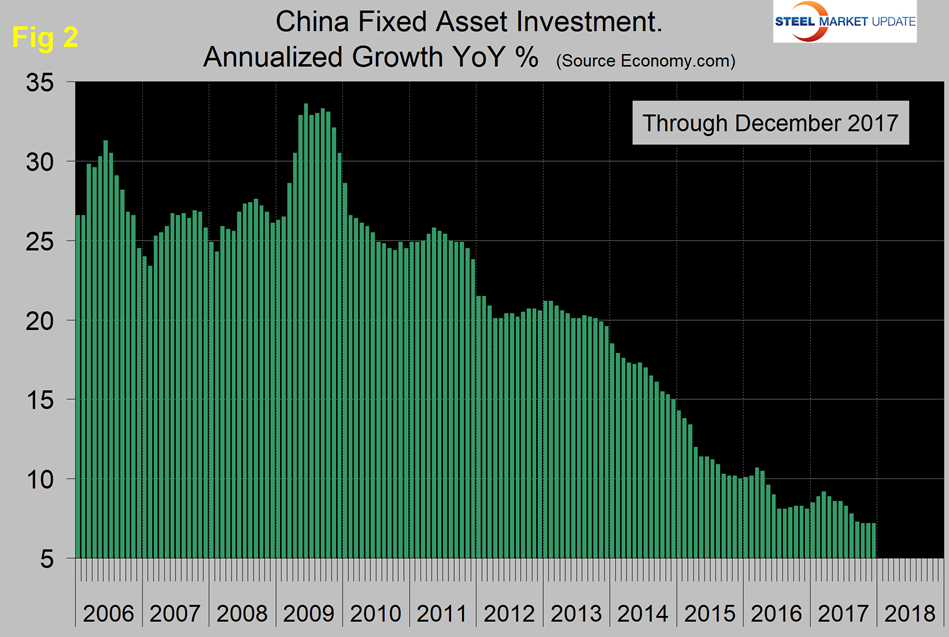

Figure 2 shows the growth of fixed asset investment year over year. In December, FAI grew at 7.2 percent, down from 9.2 percent in March. Economy.com wrote: “Chinese fixed asset investment growth steadied in December. Growth came in at 7.2 percent year over year, the same pace as in the prior month. Public investment was the main driver of investment in 2017, up a firm 10 percent year over year compared with a 6 percent lift in the private sector. However, investment has slowed noticeably since March this year, with ongoing strength in public works being partly offset by a cooling real estate sector. Since containing financial risks is one of the Chinese government’s major priorities for 2018, investment is likely to remain relatively cool in 2018.”

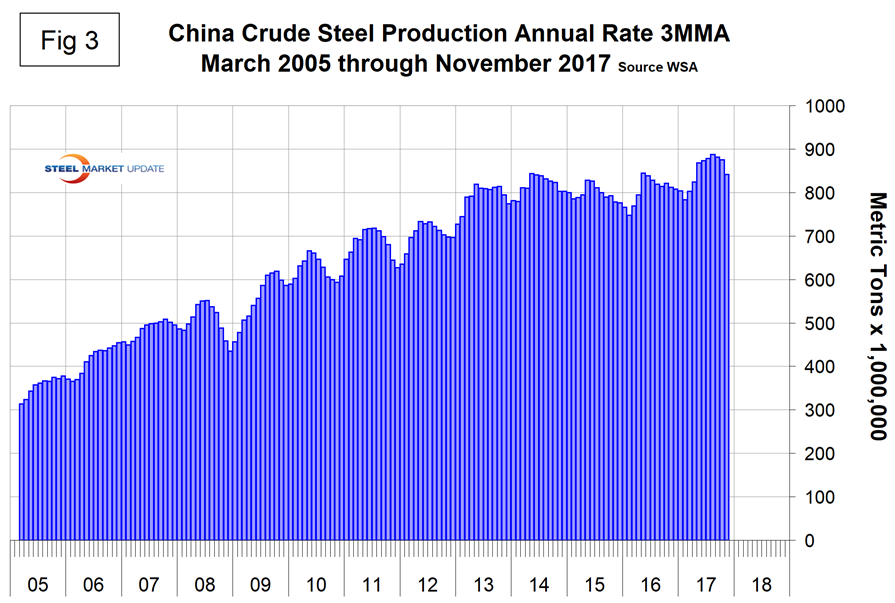

Figure 3 shows the 3MMA of China’s crude steel production through November when it accounted for 48.5 percent of global production. This was the lowest global share since February 2017. Each month, May through August set another all-time high for Chinese steel production, reaching 74.6 million metric tons in August. Production fell to 66.2 million in November. On Nov. 22, Platts reported that Tangshan, China’s biggest steelmaking city, had launched well-publicized steel output cuts the week before in an attempt to improve air quality in Beijing, Tianjin and 26 surrounding cities.

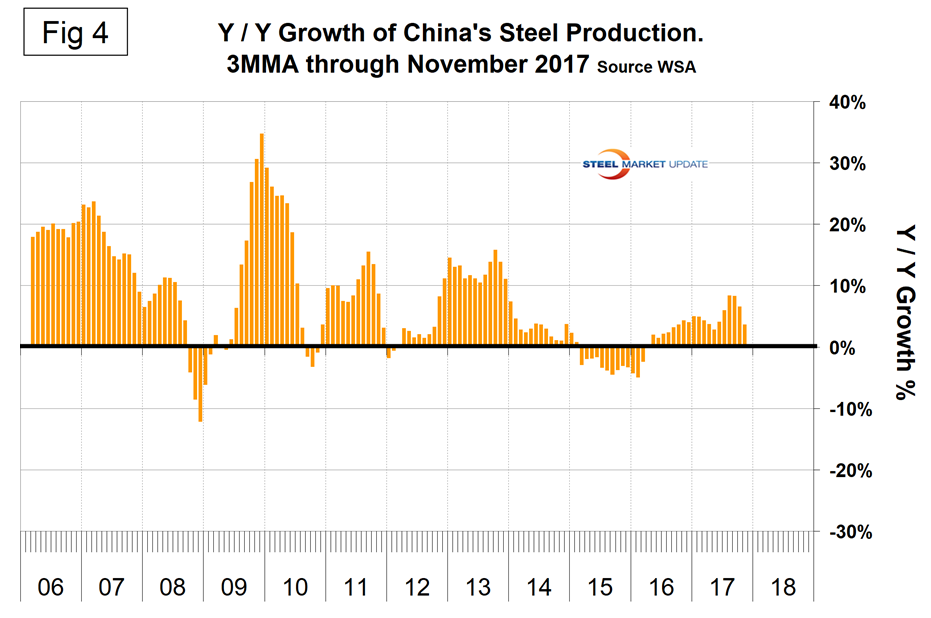

Another way of looking at the change in growth is shown in Figure 4. Growth improved from contraction in the 13 months through March last year to positive 8.4 percent in August this year, then falling to 3.6 percent in November. The central government reiterated recently that cutting overcapacity is high on its reform agenda as excess capacity in sectors such as steel and coal has weighed on the country’s overall economic performance.

In its short-range forecast released in October, the World Steel Association had this to say: “The Chinese economy, which has been gradually decelerating, is increasingly supported by consumption, while investment continues to decelerate. However, government stimuli, particularly a moderate boost to the construction program, contributed to increased GDP growth in 2017. China’s steel demand is expected to increase by 3.0 percent in 2017, an upward revision over the previous forecast. The recent closure of induction furnaces will lead to a one-off jump in measured steel use in 2017 to 12.4 percent. (This counterintuitive result arises because induction furnace output, which was previously not captured, is now being produced by the mainstream industry for which data collection is better). The outlook for China’s steel demand in 2018 remains subdued, showing no growth over 2017 as the government resumes and strengthens its efforts on economic rebalancing and environmental protection.”

SMU Comment: Despite the Chinese government’s claims that it intends to shutter excess steelmaking capacity, China’s steel production has continued to grow year over year. Capacity utilization is so low that it’s not a problem to cut production in polluted locations and to simultaneously increase production overall. The good news is that China’s steel production growth rate was less than the world’s as a whole in August through October before pulling slightly ahead again in November.