Distributors/Service Centers

September 20, 2017

MSCI: August Shipments Below Average

Written by Peter Wright

Service center shipments in August failed to perform as well as the average since 2009, according to data from the Metals Service Center Institute.

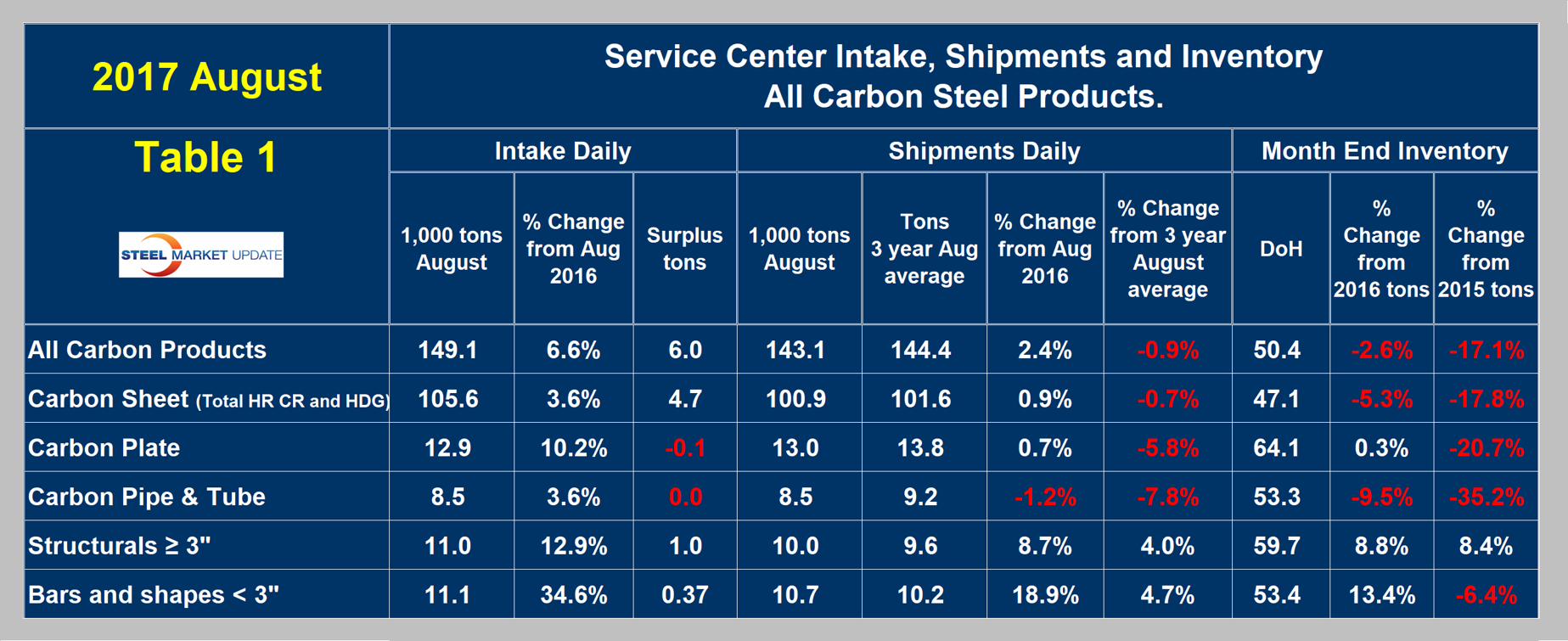

Daily shipments in August were 1.8 percent higher than in July. On average since 2009, August has increased by 3.0 percent, therefore the latest numbers were less than the historical average for this time of year. Carbon steel shipments were 143,100 tons per day in August and days on hand on the 31st averaged 50.4, almost the same as the 50.3 at the end of July.

For the first time in this analysis, we are reporting days on hand (DoH) for August. All previous updates have reported as months on hand (MoH). The problem with MoH is that it is influenced by the number of shipping days, therefore another variable is introduced. Days on hand are historically much less spiky. In August, MoH fell to 2.19 from 2.51 in July. The reason for this decline was that shipping days increased from 20 to 23, therefore total shipments for the month were elevated, which reduced the value of inventory/shipments. This problem is eliminated by considering inventory/daily shipments.

Intake and Shipments

In August, total carbon steel intake at 149,100 tons per day was 6,000 tons more than shipments. This was the third month of surplus after three months of deficit. Total sheet products had an intake surplus of 4,700 tons. This was the fourth month of surplus after three successive months of deficit.

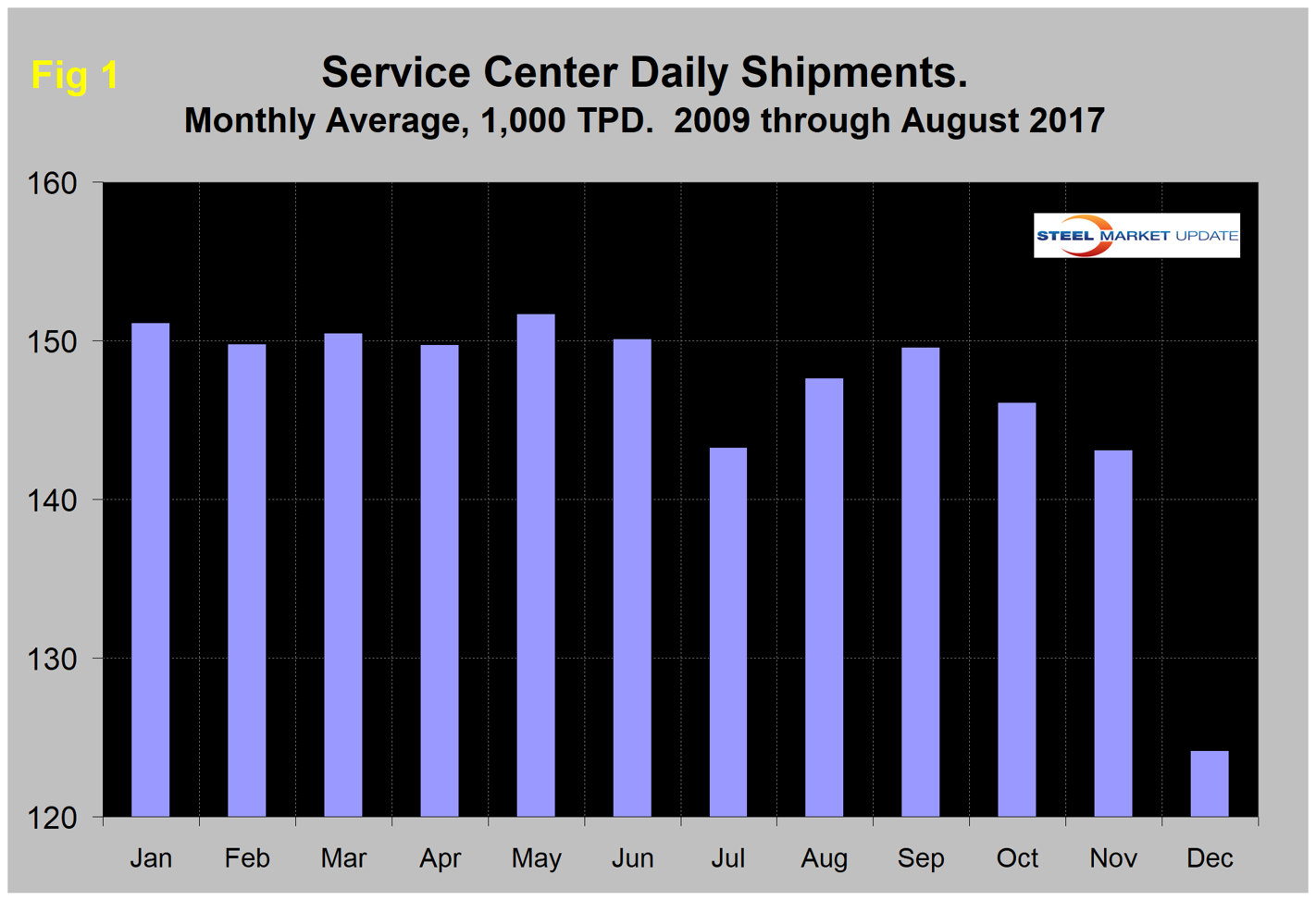

Total daily carbon steel shipments increased from 140,600 tons in July to 143,100 tons in August. MSCI data is quite seasonal, and we need to eliminate that effect before commenting in detail on an individual month’s result. Figure 1 demonstrates this seasonality and why comparing a month’s performance with the previous month can be misleading, particularly in July and the fourth quarter of the year.

We can expect shipments to increase in September, then decline every month for the remainder of the year. In the commentary below, we report year-over-year changes to eliminate seasonality and provide an undistorted view of market direction.

Table 1 shows the performance by product in August compared to the same month last year, and the average daily shipments for this and the two previous months of August. We then calculate the percent change between August 2017 and August 2016 and compare it with the most recent three-year August average.

August this year was up by 2.4 percent from August 2016, but down by 0.9 percent from the three-year August average. The fact that the y/y growth comparison is better than the three-year comparison suggests that momentum is positive.

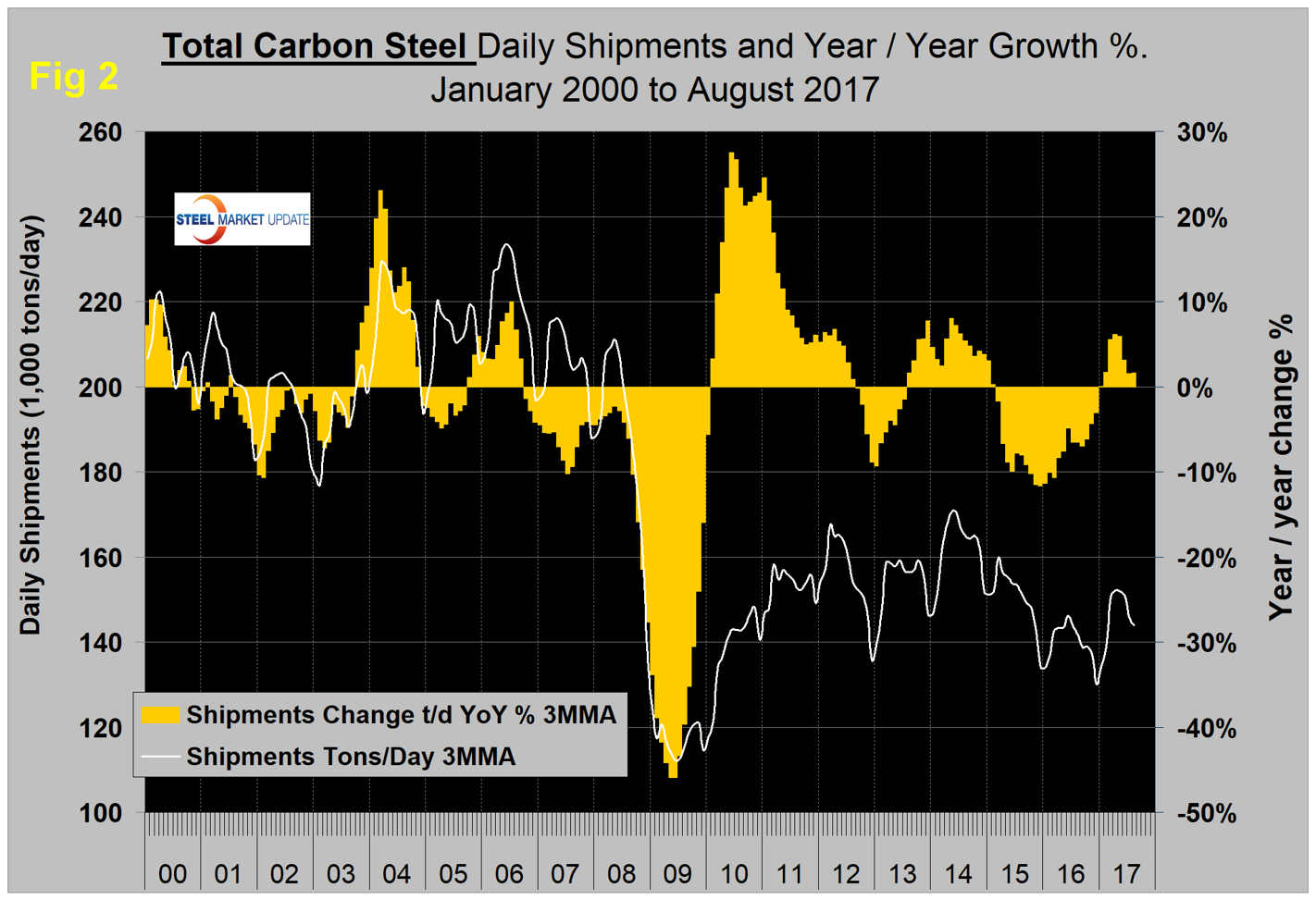

Shipments of all products except tubulars were up from August last year. Figure 2 shows the long-term trend of daily carbon steel shipments since 2000 as three-month moving averages.

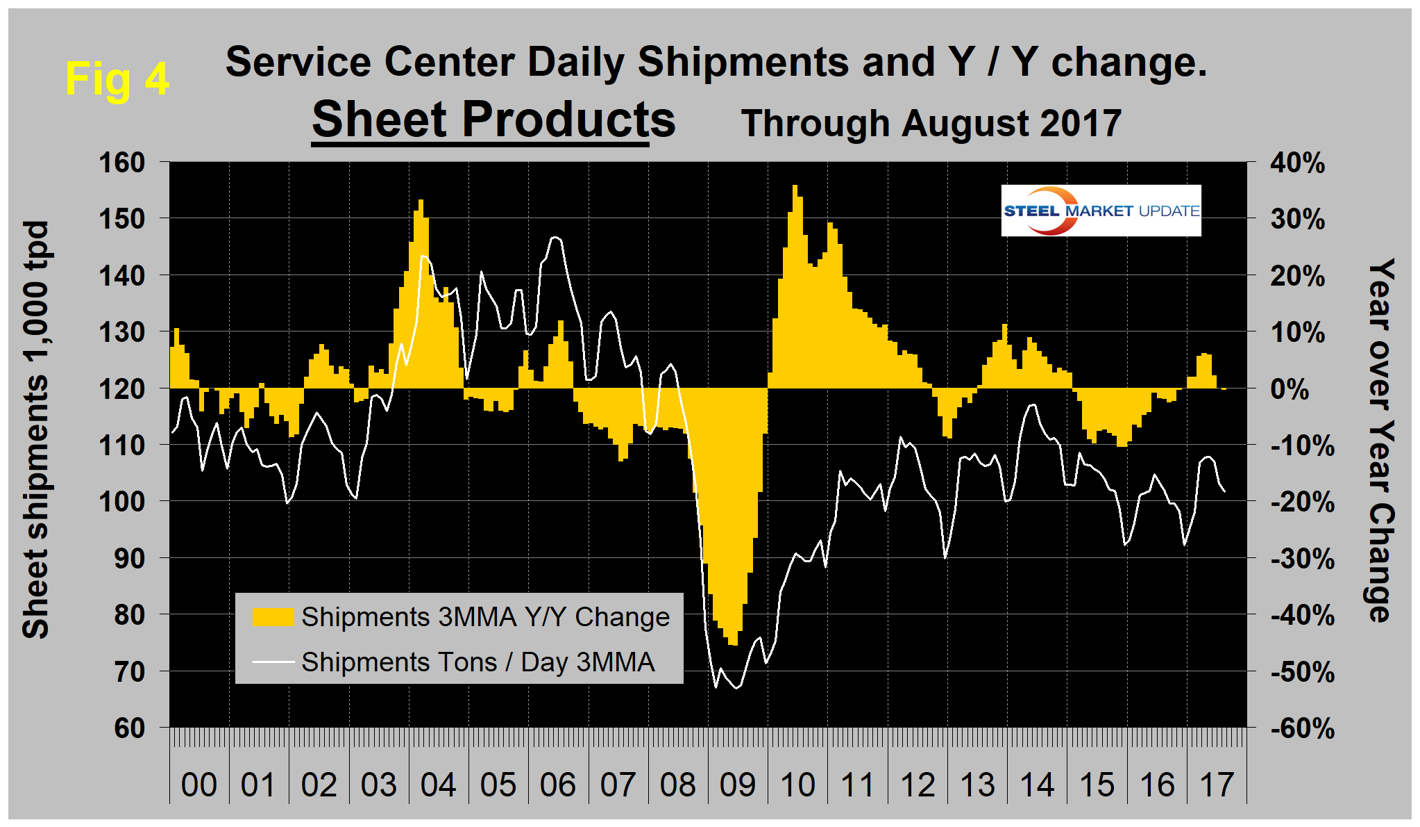

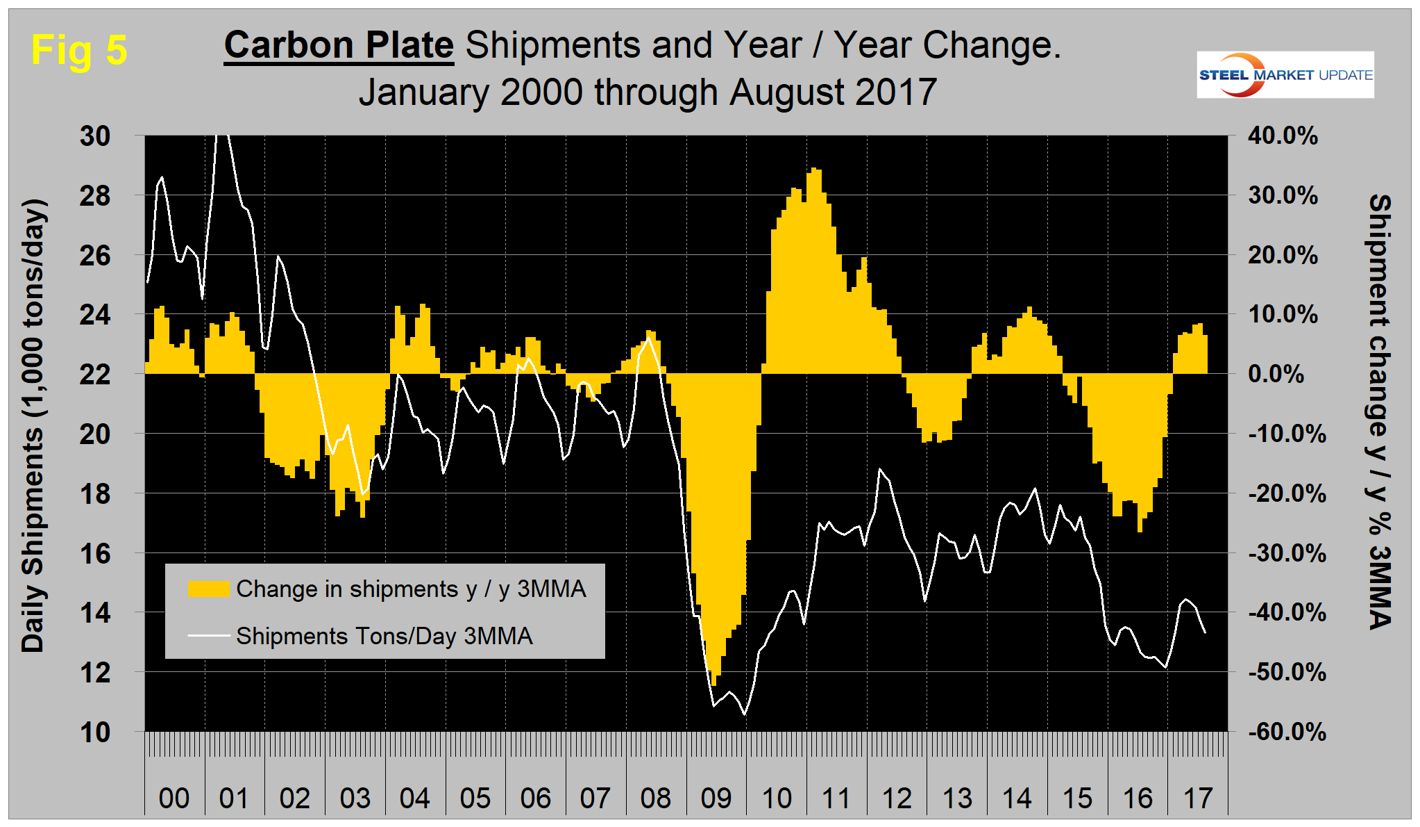

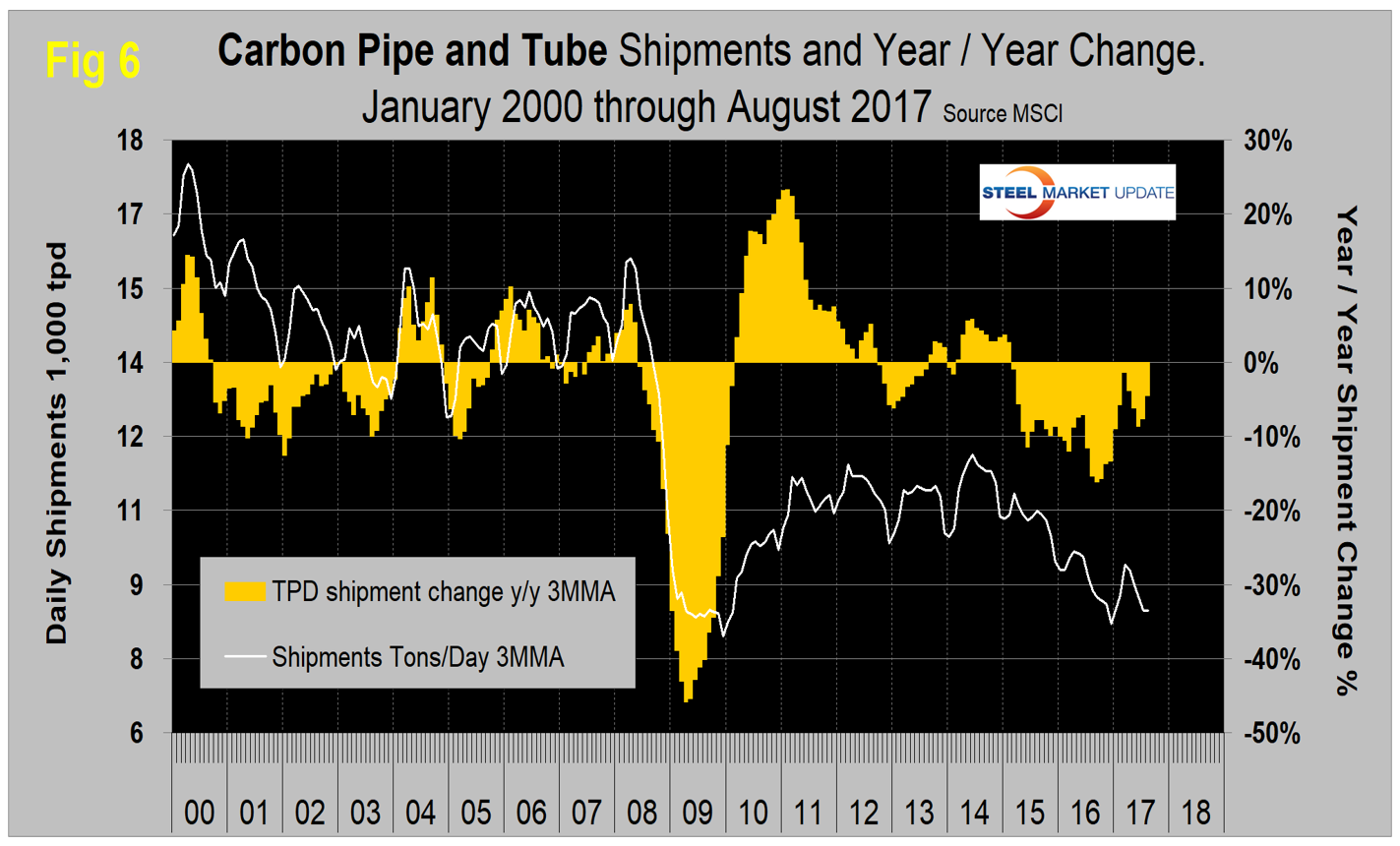

In our opinion, the quickest way to size up the market is the brown bars in Figures 2, 3, 4, 5 and 6, which show the percentage y/y change in shipments by product. In January, on a 3MMA basis, there was positive y/y growth of 0.07 percent, which improved to 6.2 percent in April before declining to positive 1.6 percent in July and August. These were the first positive y/y results since August 2015.

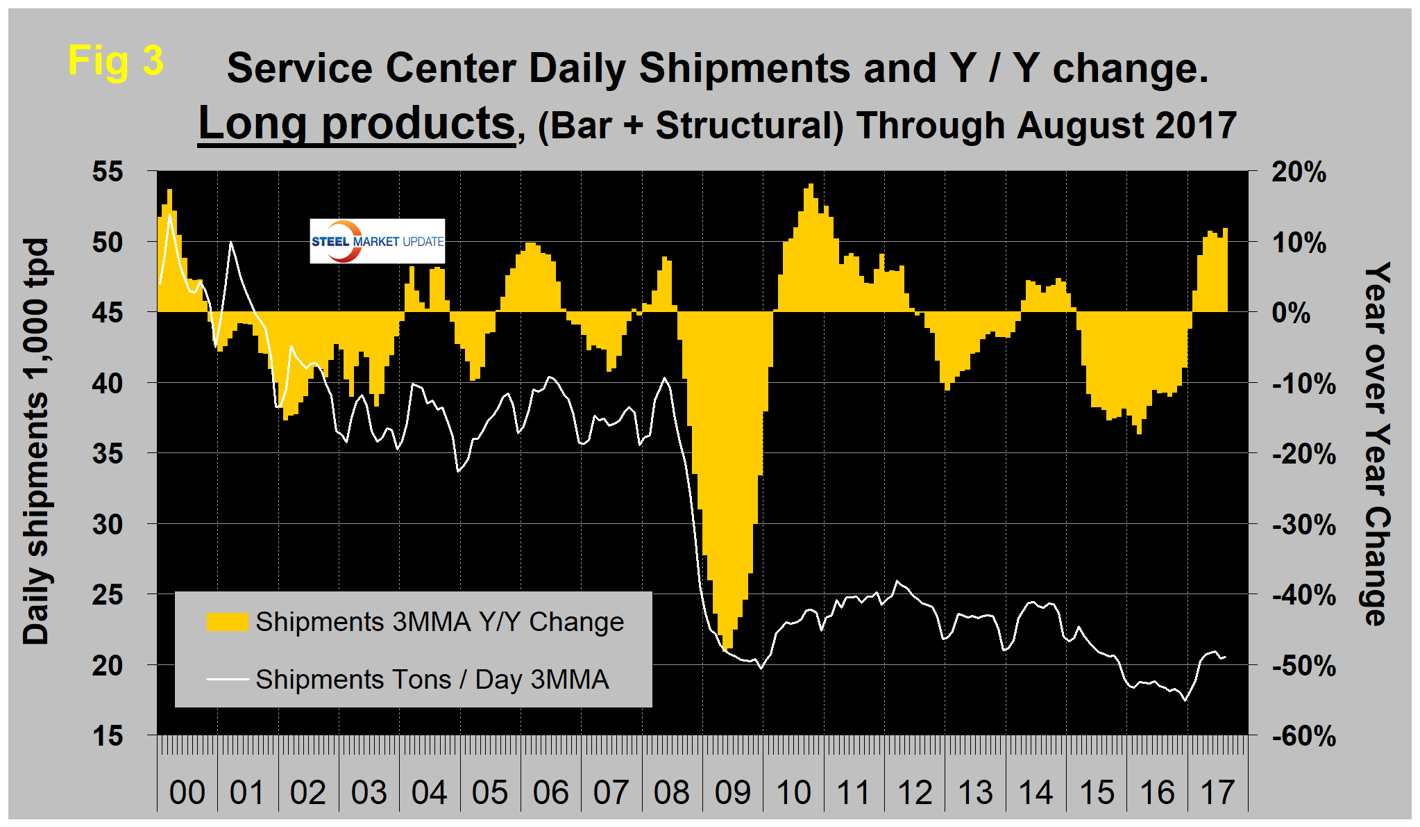

Figure 3 shows monthly long product shipments from service centers as a 3MMA with y/y change. Growth has improved this year and is now the highest it has been since early 2011. The five months through August all exceeded a 10 percent y/y growth rate.

Figures 4, 5 and 6 show the 3MMA of daily shipments and the y/y growth for sheet, plate and tubular goods, respectively. Plate performed much worse than sheet in 2015 and 2016. This year, plate has begun to close the gap. Pipe and tube have performed very poorly since early 2015, which exactly coincided with the decline in rig count. The rig count has almost doubled from this time last year, but so far this has not translated into improved shipments of pipe and tube from service centers.

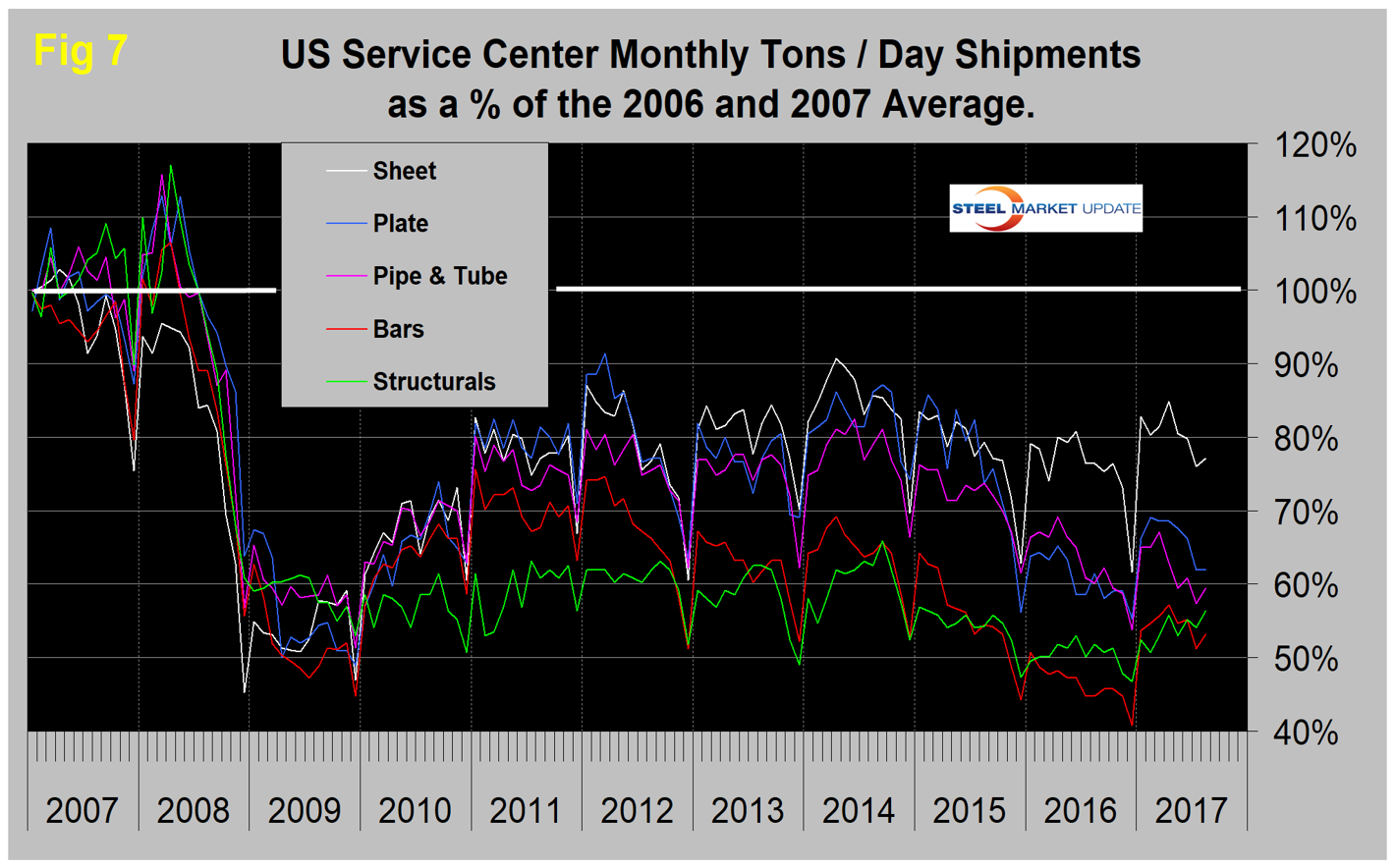

In 2006 and 2007, the mills and service centers were operating at maximum capacity. Figure 7 takes the monthly shipments by product and indexes them to the average for 2006 and 2007 to measure the extent to which shipments of each product have recovered. Each year, all products experience the December collapse and January pickup. In August, the total of carbon steel products was 67.4 percent of the shipping rate that existed in 2006 and 2007. Structurals and bar were 56.3 percent and 53.2 percent, respectively. Sheet was at 77.1 percent, plate at 61.9 percent and tubulars at 59.4 percent.

Inventories

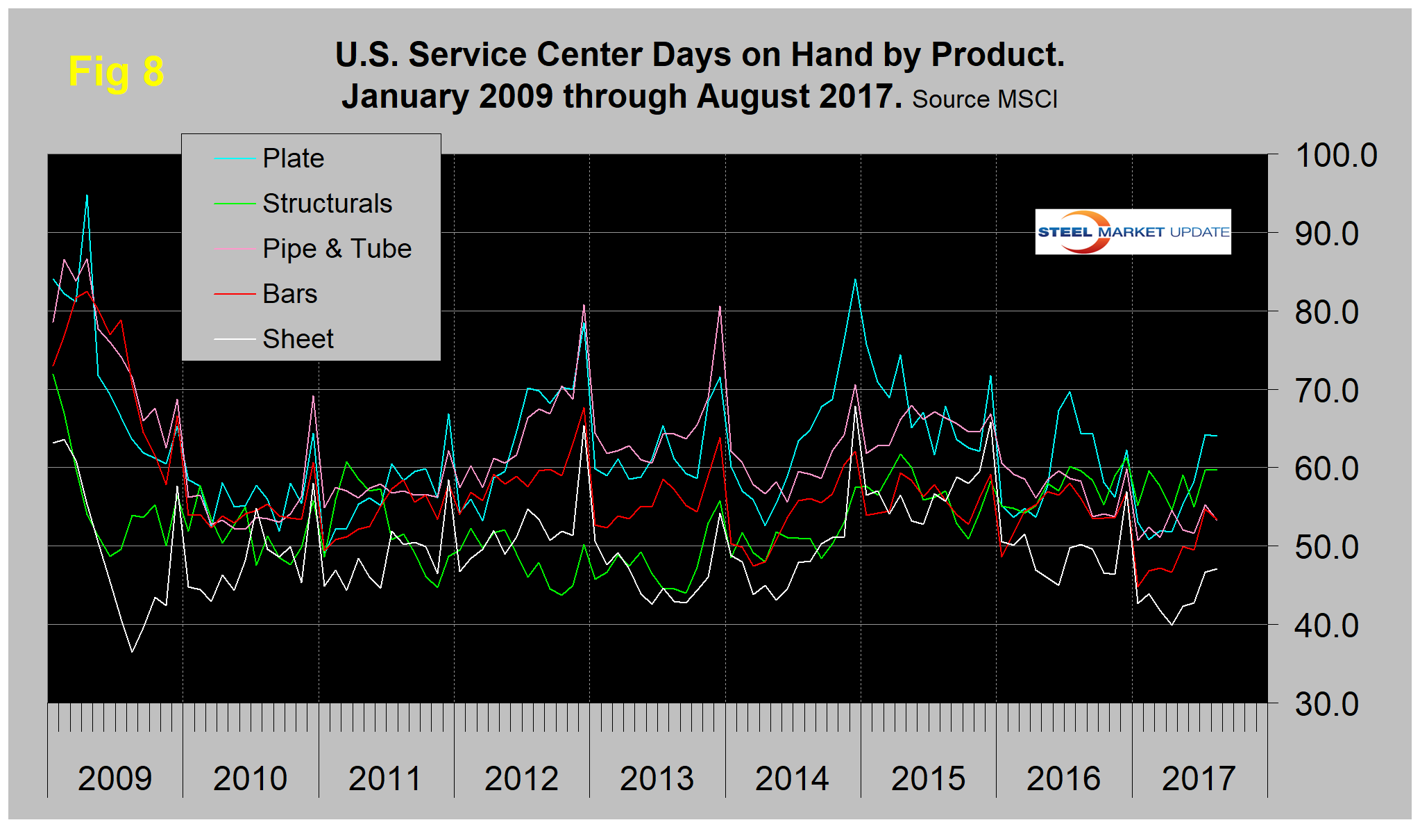

March closed with months on hand (MoH) of 1.94 for all carbon steel products, which was the lowest level in 13 years (since August 2004). This anomaly partly resulted from 23 shipping days, which was the same as August. We have now removed that effect as described above. Compared to the end of August last year, days on hand (DoH) declined from 53.0 to 50.4, but there has been an increasing trend for all products in the last five months. On a tonnage basis, total carbon steel inventories at the end of August were down by 2.6 percent y/y, led by pipe and tube, which declined by 9.5 percent. Sheet was down by 5.3 percent and plate was up by 0.3 percent. Bar-sized shapes were up by 13.4 percent. Figure 8 shows the DoH by product monthly since August 2009.

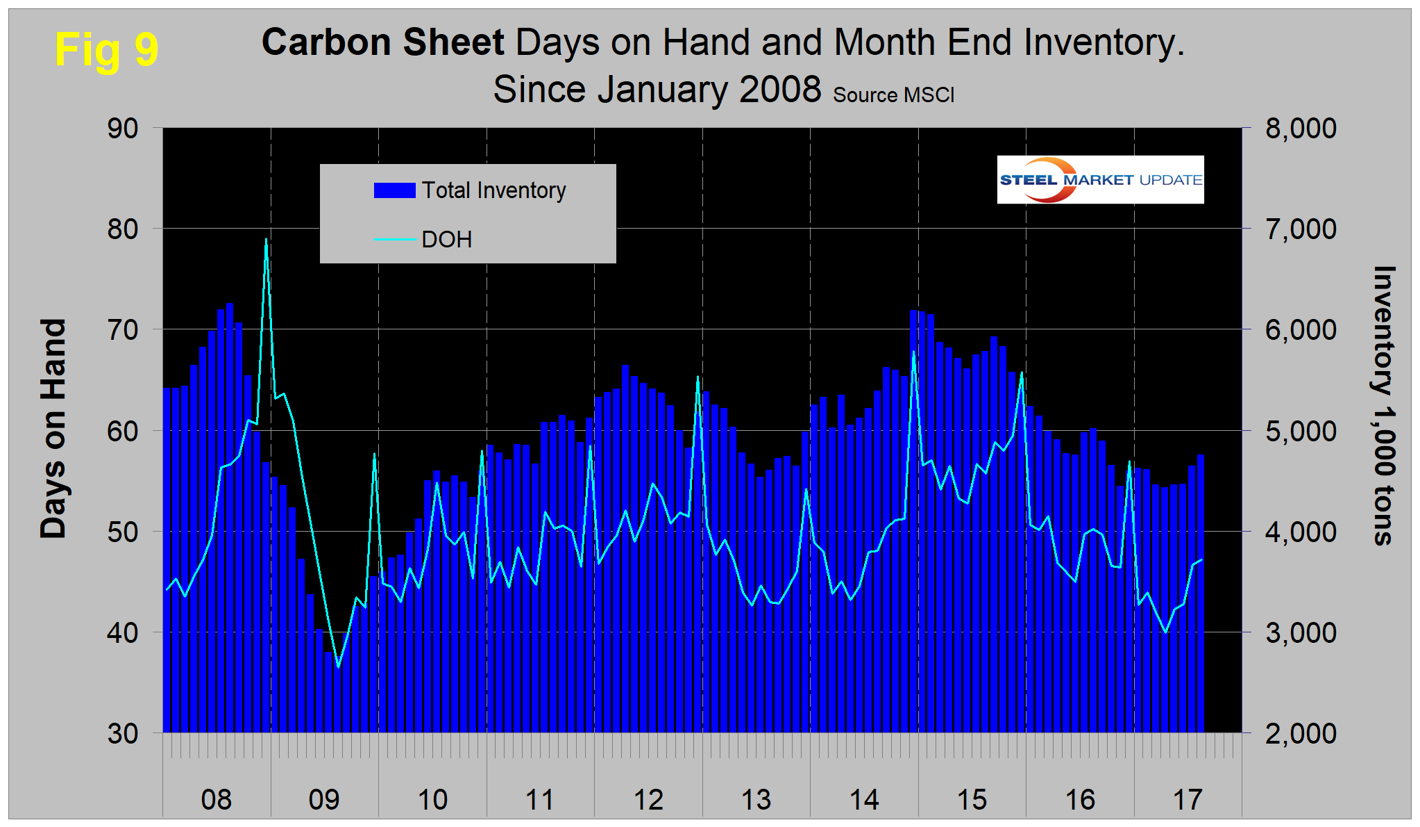

Figure 9 shows both the month-end inventory and days on hand since August 2008 for total sheet products. The total inventory tonnage of sheet products has been in decline since the end of 2014 with a possible turnaround beginning in July and August.

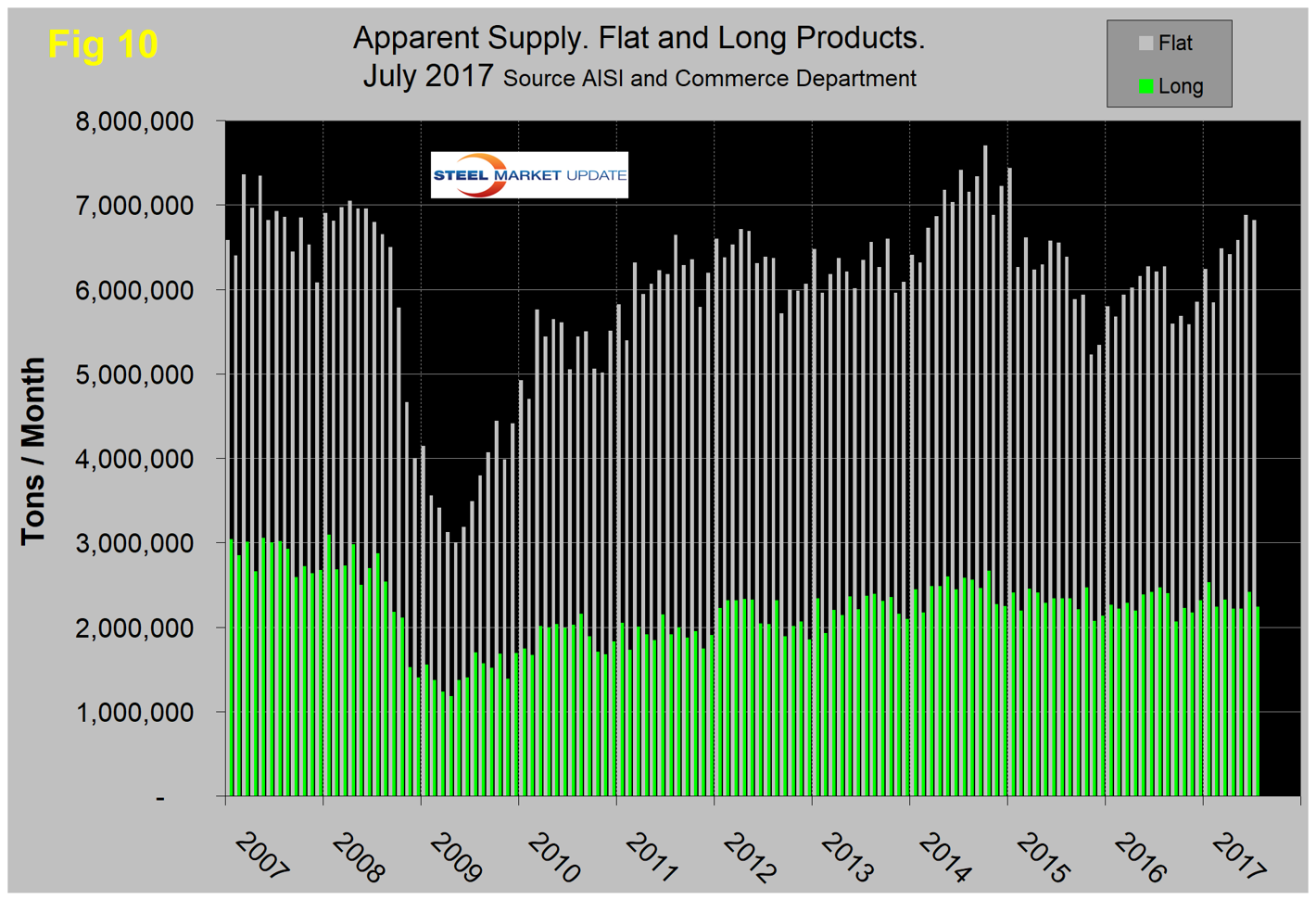

SMU Comment: In Figures 2, 3, 4, 5 and 6, the white lines show tons per day shipments on a 3MMA basis. In the first few months of 2017, there was the normal seasonal increase in total shipments as December moved out of the rolling three-month picture. However, there has been a big difference between products. Long products have enjoyed double-digit growth in the last five months, but at the other extreme tubulars have contracted every month for over two years. Plate has had quite strong growth this year and has performed much more robustly than sheet, which had slightly negative y/y growth in both July and August. These observations don’t jibe with our analysis of AISI and Commerce Department data. Figure 10 shows the total supply to the market of long and flat products based on AISI shipment and import data through July, which is the latest data available. Total supply of long products has gone nowhere since mid-2014, in contrast to the recent double-digit growth at the service center level. Flat rolled products, on the other hand, have had very strong growth in total supply to the market for the last 12 months. But because of the overriding volume of sheet, this has been muted for service centers.

The SMU data base contains many more product-specific charts than can be shown in this brief review. For each product, we have 10-year charts for shipments, intake, inventory tonnage and months on hand. Some readers have requested these extra charts for a particular product, and others are welcome to do so.