Market Data

July 31, 2017

Global Manufacturing Expands at Steady Rate

Written by Sandy Williams

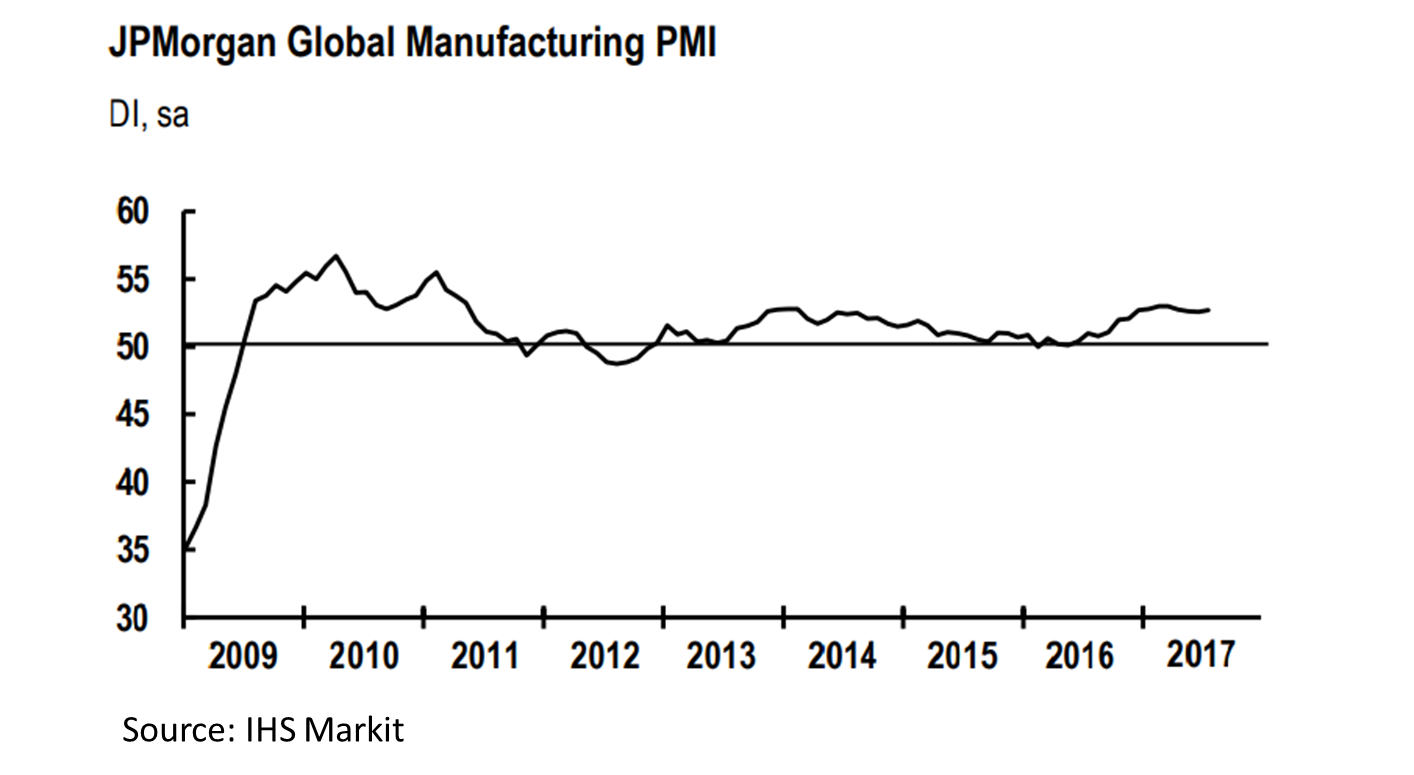

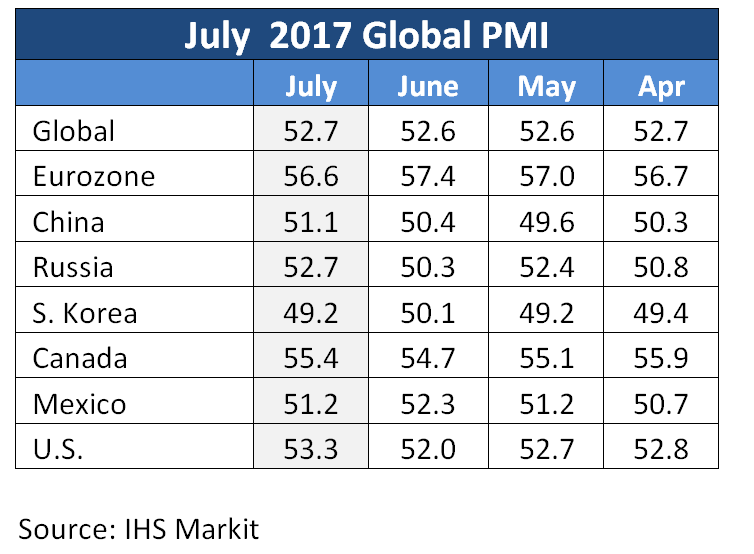

The JP Morgan Global Manufacturing PMI registered 52.7 in July indicating continued manufacturing growth across the globe. During the last four months, manufacturing expansion has remained steady at 52.6 in June and May, and 52.7 in April.

Growth in June was again led by European nations with eight of the ten best-performing countries in Europe. Canada was in fourth place and Australia in tenth. The U.S. PMI was in fourteenth position.

Input costs accelerated for the first time in six months as production expanded. Costs were passed on to clients pushing average output prices up at the fastest rate since April. Average vendor lead times were at their longest in six months.

“The global manufacturing sector achieved further solid and steady growth during July,” commented David Hensley, Director of Global Economic Coordination at JP Morgan. “Although the rate of output expansion eased slightly, stronger inflows of new business and rising workforce numbers suggest that the current pace of increase should be broadly sustained going forward. Cost pressures saw a slight move higher though, as sustained growth stretched global supply chains and led to increased raw material prices.”

Eurozone

Manufacturers in the Eurozone saw some moderation in the rate of business expansion in July. The IHS Markit Manufacturing PMI dipped to 56.6 from a 74-month high of 57.4 in June. All eight of the countries in the region experienced broad-based growth with the strongest conditions in Austria, the Netherlands and Germany. Orders, both domestic and export, expanded in July, although at a slower rate. Backlogs increased for the 27th month and supplier delivery times lengthened to the greatest degree since April 2011. Employment rates increased in response to production needs. Price pressures eased in July and, despite increased raw material prices, a sellers’ market developed for a number of purchased goods, said IHS. The 12-month view for production volumes was relatively optimistic for all countries except Italy and Ireland.

China

Output and new orders rose at a quicker pace in July for Chinese manufacturers, helped by an increase in new export sales. Export sales increased at their second-fastest rate since September 2014. The Caixin China General Manufacturing PMI rose to 51.1, up from 50.4 in June. Production rose to meet demand, but workforce numbers declined, adding to backlogs of work. Purchasing activity increased in July for a marginal increase in stocks of raw material inventories. Input costs increased at the fastest rate in four months with higher prices on raw materials mentioned in the PMI survey. Prices for finished products grew for the second month. Twelve-month optimism was somewhat weaker in July.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, expects the rise in buying activity to lead to moderate growth in manufacturing production going forward. “Operating conditions in the manufacturing sector improved further in July, suggesting the economy’s growth momentum will be sustained. That said, it’s unlikely that financial regulatory tightening will be relaxed.”

Russia

Manufacturing conditions quickened their upward pace in July driven by strong rates of expansion in output and new orders. Backlogs increased at the fastest pace since January 2003 and input and output price inflation eased. The PMI rose to 52.7 from 50.3 in June. Business outlook remained positive in July, but fell to its lowest level since January 2016. IHS Markit predicts industrial production will grow 2.4 percent year-over-year in the second quarter and 2.0 percent overall for 2017.

South Korea

South Korea saw a sharp reduction in output in July as export orders fell for their sixth month. Orders were filled when possible by warehouse inventories, adding a fourth month of contraction for finished goods. Export activity was particularly weak from China and Japan. Although manufacturers are forecasting business growth for the next 12 months, optimism was at its lowest point since April. The PMI in July slipped into contraction to 49.2 from June’s reading of 50.1.

Mexico

Manufacturing activity in Mexico softened in July as weaker client demand put the brakes on production and new order growth. The PMI slipped to 51.2 from 52.3 in June. New export orders decreased marginally, ending an 11-month upward trend. Hiring increased in July as manufacturers worked through backlogs and looked forward to long-term expansion plans. Growth was forecast for the next 12 months by about half of survey respondents with only 7 percent expecting declining conditions. Confidence remained well above levels seen at the beginning of 2017.

Canada

Canadian manufacturers experienced a surge in business activity in July. Production grew at the fastest rate since March as new orders improved and input cost inflation moderated to a nine-month low. Survey responses indicated new order growth was due to increased domestic spending. Forty percent of those surveyed expect output volumes to expand in the year ahead. The IHS Markit Canada Manufacturing PMI rose to 55.5 from 54.7 in June.

Tim Moore, Associate Director at survey compilers IHS Markit, noted, “July data highlighted that Canada’s manufacturing sector maintained an impressive growth rate, as production volumes rose to the second-largest extent since November 2014. Stronger domestic demand was the key factor boosting manufacturing growth in July, reflecting improving economic conditions and rising sales to energy sector clients.”

United States

The IHS Markit U.S. Manufacturing PMI registered 53.3 in July, up from 52.0 in June. Output and new orders grew at a solid pace in July as client demand accelerated. Export orders dropped slightly, decreasing for the first time in 10 months. Inventories for both input and finished products increased in July. Input costs rose modestly along with output prices, and backlogs fell. Workforce expansion was the strongest in five months and confidence in future business activity was at a six-month high.

“Although rising, the survey indices remain consistent with only very modest increases in comparable official data such as manufacturing output, durable goods orders and payroll numbers,” said Chris Williamson, Chief Business Economist at IHS Markit. “Clearly, the manufacturing sector remains stuck in a low gear, though it’s at least gaining momentum and will hopefully shift up a gear as we move through the second half of the year, if demand continues to improve. IHS Markit expects GDP growth to accelerate to a near 3 percent annualized rate in the third quarter, fueled by gains in consumer spending and business investment, which should benefit manufacturing.”