Market Data

December 8, 2016

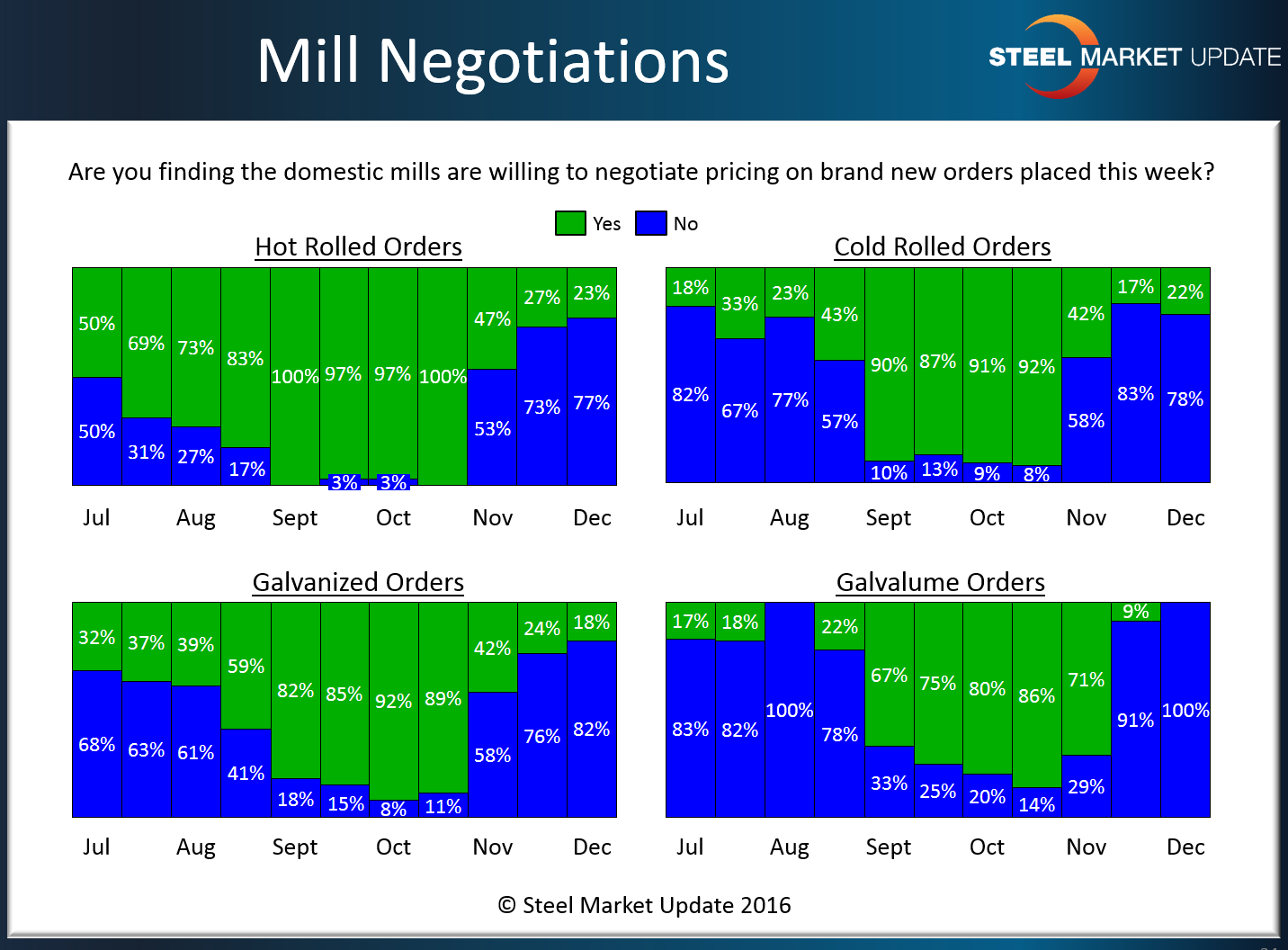

Steel Mills Taking Much Firmer Stand on Steel Price Negotiations

Written by John Packard

According to those participating in this week’s flat rolled steel market trends survey the domestic steel mills are taking a firm stance to price negotiations. Since the first price increase announcements were made in late October the percentage of steel buyers reporting the mills as willing to negotiate prices has dropped from a high of 100 percent on hot rolled in mid-October to only 23 percent today.

We are seeing similar results with other flat rolled products as well.

The percentage of buyers reporting the mills as willing to negotiate cold rolled prices dropped from 92 percent in mid-October to 22 percent this week.

Only 18 percent of our respondents reported the mills as willing to negotiate galvanized pricing. In mid-October that number was 86 percent.

Galvalume was even more impressive as zero percent of our respondents reported the mills as willing to negotiate AZ pricing. In mid-October that number was 86 percent.

The less willing the mills are to negotiate pricing the firmer prices become.

A side note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.