Analysis

October 6, 2016

Construction Expenditures through August 2016

Written by Peter Wright

Each month the Commerce Department issues its Construction Put in Place (CPIP) data, usually on the first working day covering activity two months earlier. August data for CPIP was released on Monday October 3rd.

![]() Overall this was a disappointing report with the growth of total construction having declined for five consecutive months and continuing to have negative momentum. Of the three funding categories, private, state & local and federal, only private work had positive growth in three months year over year and that with a slowing trend. All four construction sectors had negative momentum. These are non-residential buildings, residential buildings, infra-structure and other which is a catch all for industrial, utilities and power.

Overall this was a disappointing report with the growth of total construction having declined for five consecutive months and continuing to have negative momentum. Of the three funding categories, private, state & local and federal, only private work had positive growth in three months year over year and that with a slowing trend. All four construction sectors had negative momentum. These are non-residential buildings, residential buildings, infra-structure and other which is a catch all for industrial, utilities and power.

At SMU we analyze the CPIP data with the intent of providing a clear description of activity that we believe accounts for over 30 percent of total steel consumption. Please see the end of this report for more detail on how we perform this analysis and structure the data but in particular note that we are presenting NONE seasonally adjusted numbers. Much of what you will see in the press may differ from what we are presenting here because others are basing their comments on adjusted values. Our rational is that construction is highly seasonal and our businesses function in a seasonal world. Also we don’t understand how the adjustments are made neither do we trust them.

Total Construction

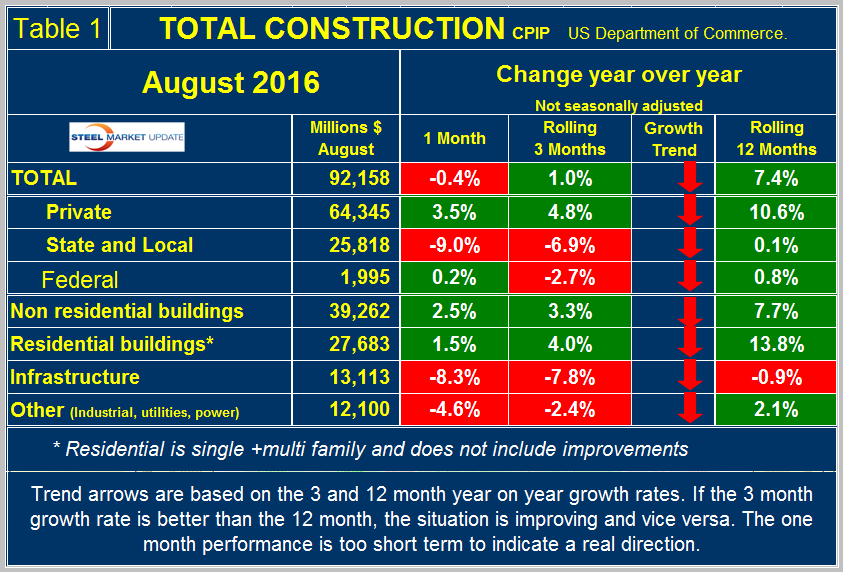

Total construction grew by 1.0 percent in three months through August year over year. There has been a steady decline since the 12.4 percent growth achieved in March. On a rolling 12 months basis construction expanded y/y by > 10 percent for eleven consecutive months through June then declined to 9.9 percent in June, 8.8 percent in July and 7.4 percent in August. It is evident that growth is slowing as momentum has been negative for the last five months. All growth measures included below are on a 3MMA basis year over year which is our way of eliminating seasonality.

August total construction expenditures were $92.158 billion which breaks down to $64.3 B of private work, $25.8 B of state and locally (S&L) funded work and $2.0 B of federally funded (Table 1).

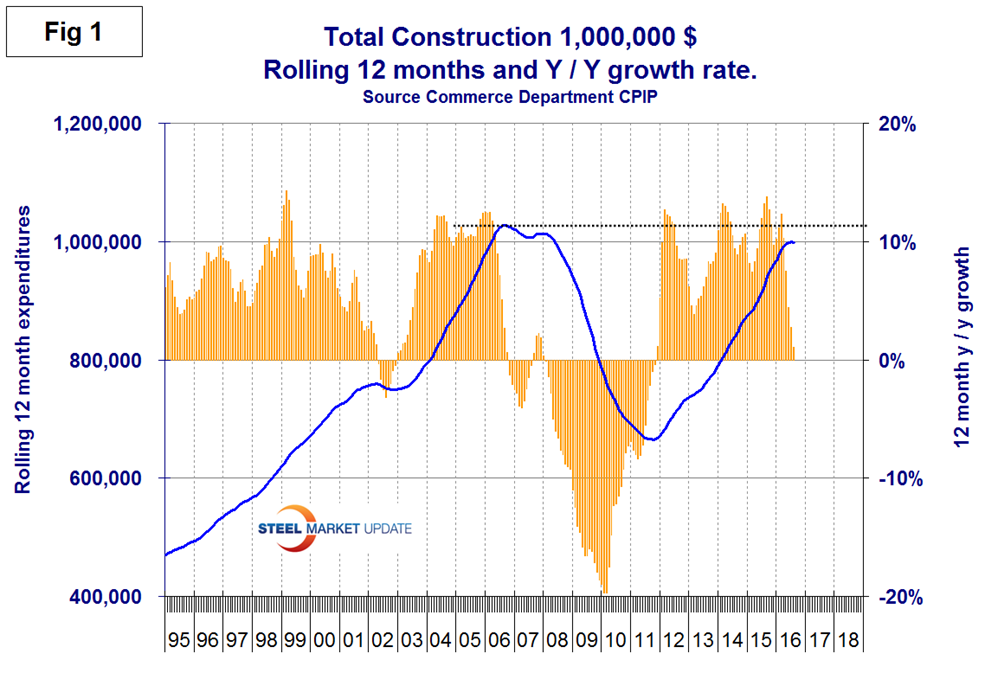

The red and green arrows in all four tables in this report show momentum. August on a 3MMA basis had an increase in year over year growth of 1.0 percent which was lower than the 7.4 percent growth on a rolling 12 months basis. This means that the growth rate has negative momentum. In our recent construction updates we expressed the opinion that total construction would reach the pre-recession level by the end of this year. It doesn’t look as though this remains true as total expenditures have leveled off (Figure 1).

The 1.0 percent growth of total construction y/y was led by private work up by 4.8 percent and pulled down by state and locally financed work with negative 6.9 percent growth and federal with negative 2.7 percent growth. Momentum was negative for all three finance channels. We consider four sectors within total construction. These are non-residential, residential, infrastructure and other which is a catch all and includes industrial, utilities and power. All four of these sectors had negative momentum in August. The growth rate of “Other” became very negative at the time of the oil price collapse but had nine straight months of positive growth through June before logging negative 0.2 percent in July and negative 2.4 percent August. The growth rate of total construction is shown by the brown bars in Figure 1. The pre-recession peak of total construction on a rolling 12 month basis was $1,028 B in 12 months through September 2006. The low point was $665.1 B in 12 months through October 2011. The 12 month total through the latest data of August 2016 was $998.780 B. June 2015 through August 2016 were the first months to exceed $900 B since March 2009 when the recession was gaining traction.

Private Construction

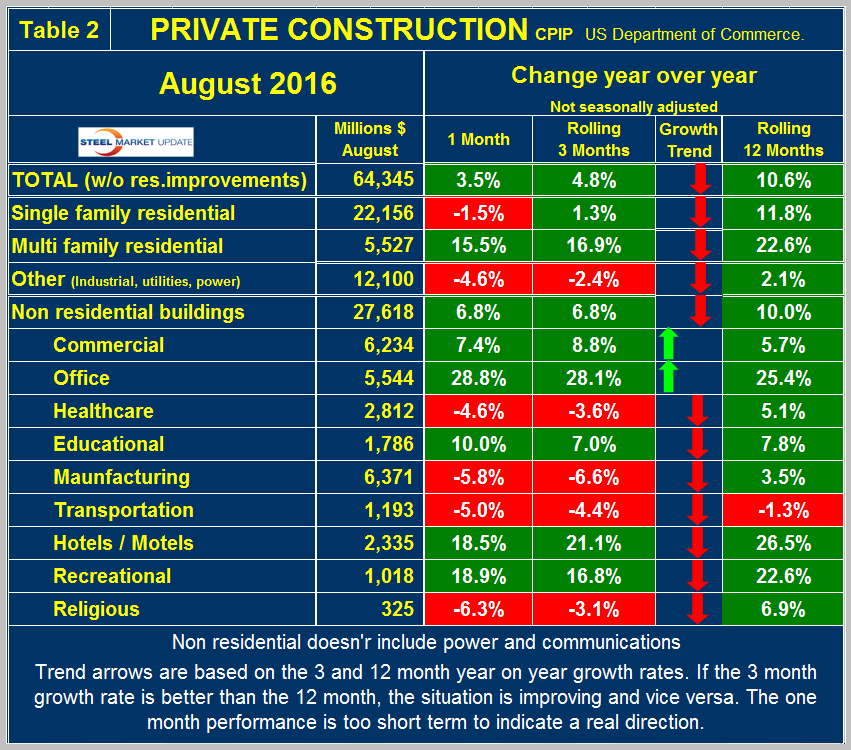

Table 2 shows the breakdown of private expenditures into residential and non-residential and subsectors of both.

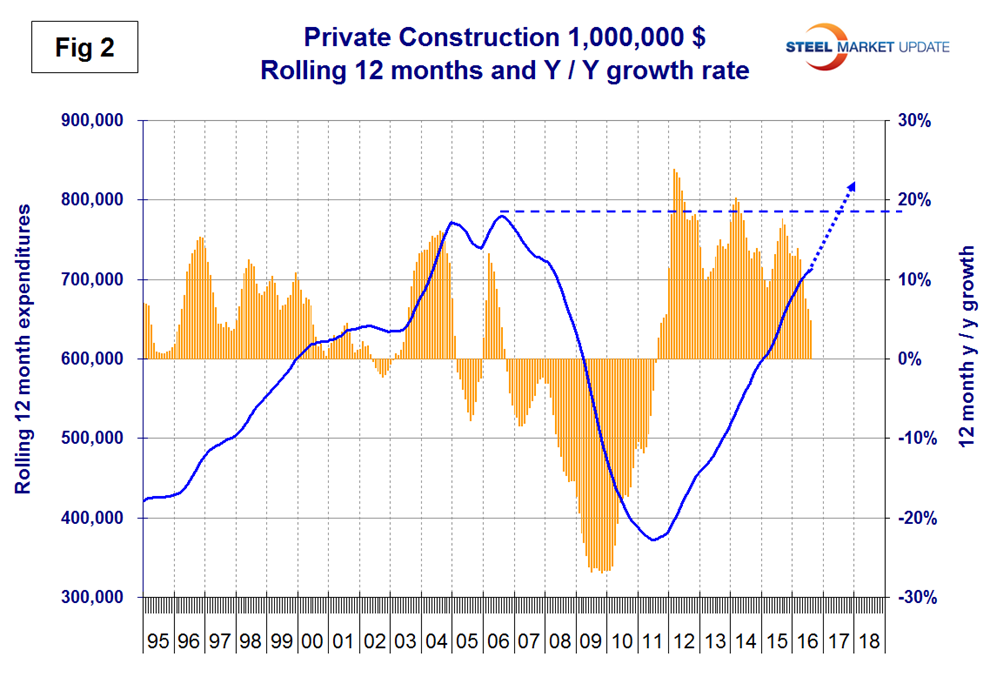

The growth rate of private construction was 4.8 percent in the three months through August as shown by the brown bars in Figure 2.

The blue lines in all four graphs in this report are 12 month totals which smooths out seasonal variation. Excluding property improvements our report shows that single family residential grew by 1.3 percent and multi-family residential is still surging with a 16.9 percent growth rate. The growth of single family construction expenditures reported here is similar to the 3.5 percent growth of starts reported by the Census Bureau. (In the starts data the whole project is entered to the data base when ground is broken). However multi family is very different. In this CPIP report multifamily expenditures grew by 16.9 percent but starts data from the Census Bureau contracted by 1.4 percent. It remains to be seen whether this difference portends a future collapse in multifamily. Within private non-residential, all sectors except commercial and offices had negative momentum. Offices, hotels/motels and recreation had strong year over year growth though as indicated by negative momentum, the latter two are slowing. The third quarter Federal Reserve Senior Loan Officer Survey indicated that there is currently a net increase in demand for construction and land development loans but that terms are tightening. This survey reviews changes in the terms of, and demand for, bank loans to businesses on a quarterly basis based on the responses from 73 domestic banks and 24 U.S. branches and agencies of foreign banks.

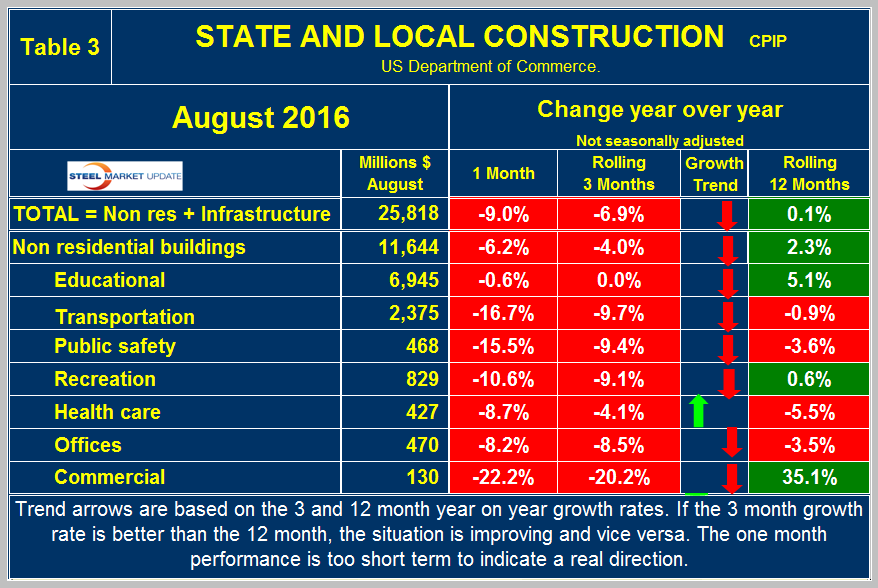

State and Local Construction

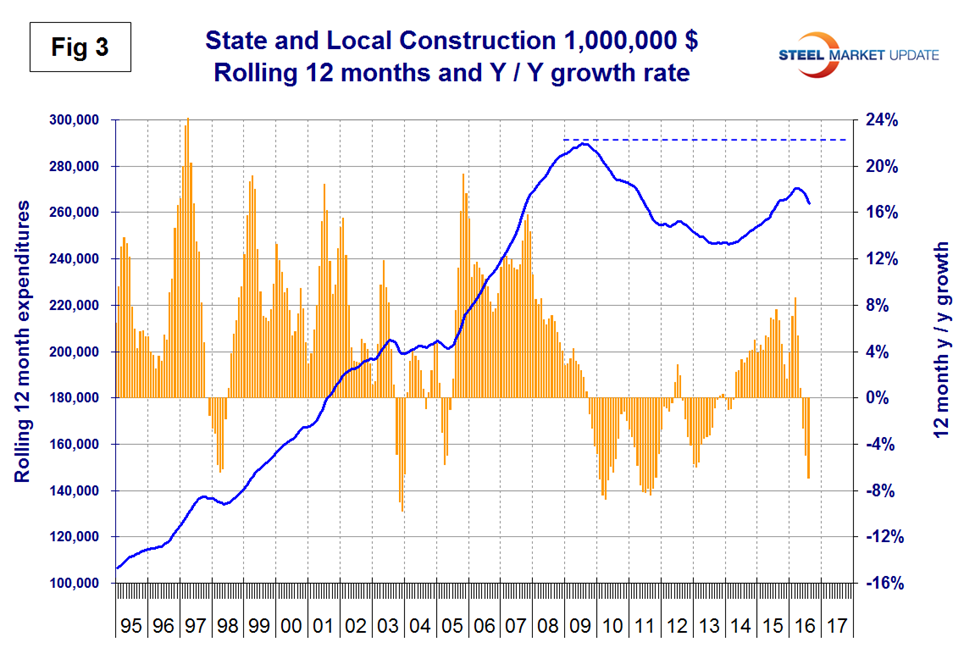

S&L work contracted by 6.9 percent in the rolling three months through August y/y with negative momentum (Table 3).

This was a deterioration from -2.7 percent in June which was the first month of contraction since April 2014. Figure 3 shows year over year growth as the brown bars and the rolling 12 month total of expenditures as the blue line.

Educational buildings are by far the largest sub sector of S&L non-residential at $6.9 billion in August and on a 3MMA basis y/y had a very slight negative growth, down from positive 14.2 percent in March. August was the first contraction in S&L educational construction expenditures since April 2014. There were no sectors within S&L with positive growth in August and all were deteriorating as shown by negative momentum. Comparing Figures 2 and 3 it can be seen that S&L construction did not have as severe a decline as private work during the recession and that private work bounced back faster. Private expenditures still have a chance of exceeding the pre-recession high next year but the downturn in S&L means that a full recovery may be delayed until the next decade.

Drilling down into the private and S&L sectors as presented in Tables 2 and 3 shows which project types should be targeted for steel sales and which should be avoided. There are also regional differences to be considered for which data is not available from the Commerce Department.

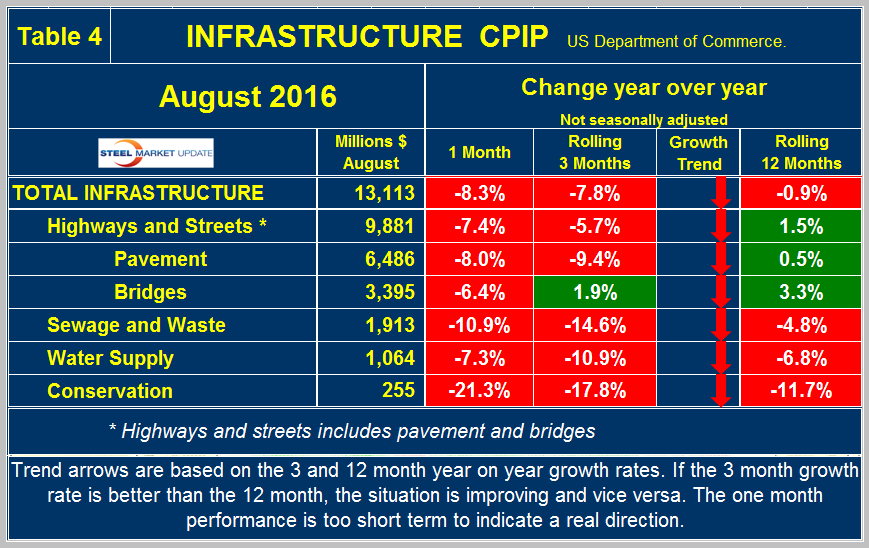

Infrastructure

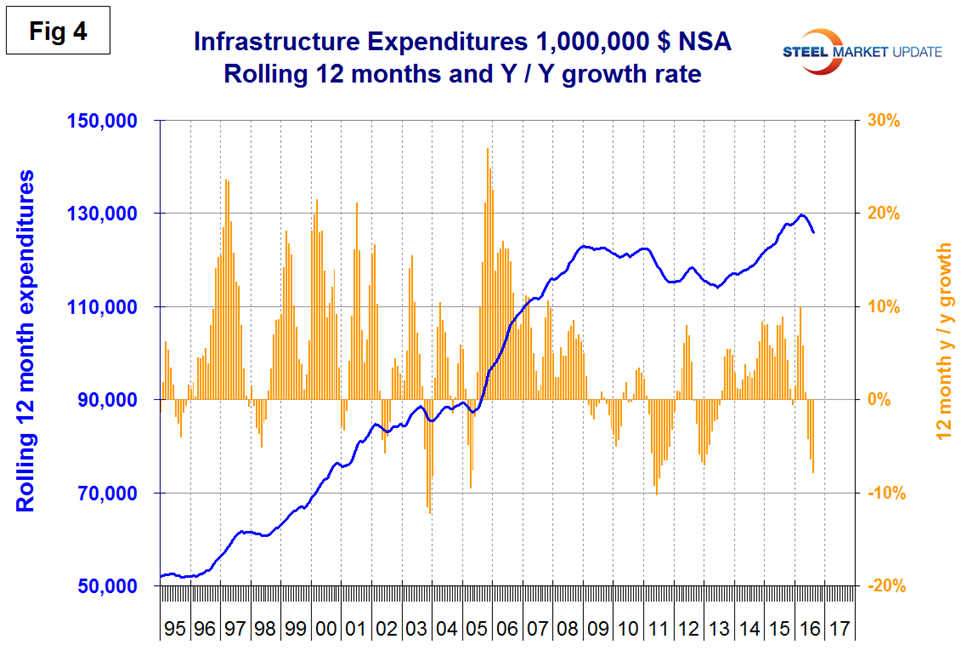

Expenditures have contracted for five straight months through August when growth was negative 7.8 percent. Prior to June there was a string of 34 out of 35 months with positive growth. Growth has slowed from a nine year high of positive 10.0 percent in March this year. Highway and streets including pavement and bridges account for about 2/3 of total infrastructure expenditures and had positive growth every month since August 2013 before contracting by 2.3 percent in June, 3.7 percent in July and 5.7 percent in August this year. Highway pavement is the main sub-component of highways and streets and had a 9.4 percent negative growth in three months through August. Bridge work had positive growth of 1.9 percent in August (Table 4).

Science Daily described a research program into steel bridge piers on October 3rd. Civil engineers at Purdue University are leading a project with the Indiana Department of Transportation to learn how to use a type of bridge pile often seen in offshore applications, research that could help reduce the cost of bridge building or replacement of aging spans.

The piles will be used in the foundations of a bridge spanning the Wabash River near the Purdue campus on the eastbound side of Sagamore Parkway in West Lafayette, Indiana. Called large open-ended pipe piles (LOEPPs), the lengths of steel pipe about 100 feet long and two feet in diameter will make up the bridge’s center piers. One advantage of pipe piles is that they can be driven into the riverbed’s alluvial soil easier than the traditional closed-ended piles, which will be used for the end piers, said Rodrigo Salgado, the Charles Pankow Professor in Civil Engineering in Purdue’s Lyles School of Civil Engineering.

Infrastructure expenditures were slow to respond to the recession due to the magnitude of many of these projects. Growth stopped in 2009 and 2010 but it wasn’t until 2011 that an actual contraction occurred. Infrastructure expenditures have exceeded the pre-recession high every month since May 2015 but are now clearly in a downturn (Figure 4).

It looks as though the passage in late December of the congressional bill for $305 billion to fund roads, bridges, and rail lines has not kicked in yet due the long planning and permitting processes for such projects. The five-year infrastructure bill is the longest reauthorization of federal transportation programs that Congress has approved in more than a decade, ending an era of stopgap bills and half-measures that left the Highway Trust Fund nearly broke and frustrated local governments and business groups.

Total Building Construction Including Residential

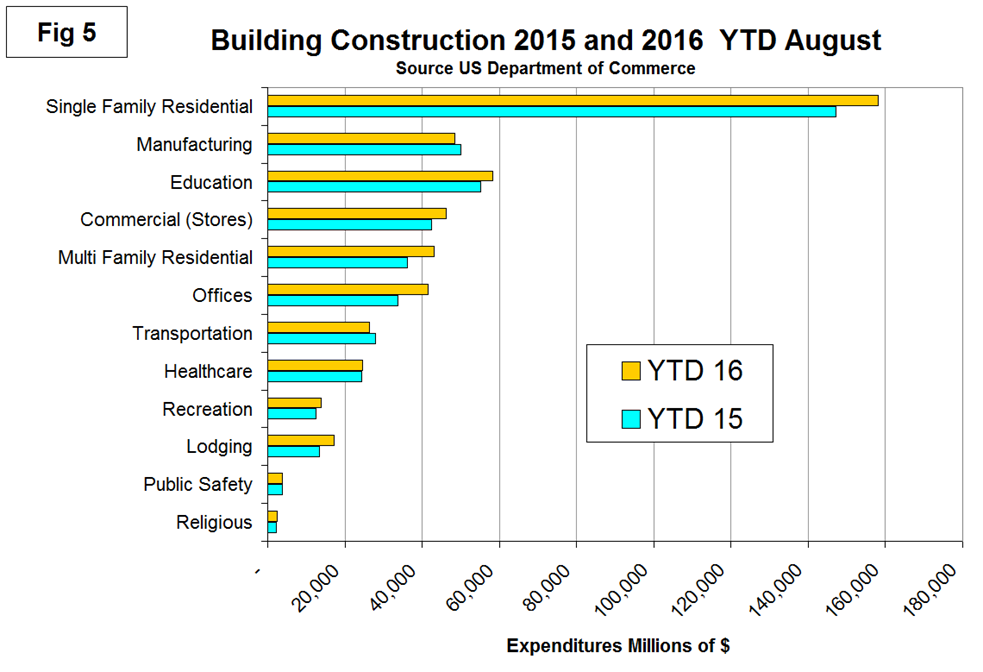

Figure 5 compares YTD expenditures for building construction for 2015 and 2016.

Single family residential is dominant and in the first eight months of 2016 totaled $158 billion, up from $147.2 billion in the same period last year. Manufacturing, transportation and public safety have contracted in the first eight months of 2016 compared to the same period last year. All other sectors are doing better led by lodging (hotels and motels) which was up by 27.1 percent followed by offices up by 22.9 percent and multi-family residential buildings up 19.0 percent.

Explanation: Each month the Commerce Department issues its construction put in place (CPIP) data, usually on the first working day covering activity two months earlier. Construction put in place is based on spending work as it occurs, estimated for a given month from a sample of projects. In effect the value of a project is spread out from the project’s start to its completion. This is different from the starts data published by the Census Bureau for residential construction, by Dodge Data & Analytics and Reed Construction for non-residential and Industrial Information Resources for industrial construction. In the case of starts data the whole project is entered to the data base when ground is broken. The result is that the starts data can be very spiky which is not the case with CPIP.

The official CPIP press release gives no appreciation of trends on a historical basis and merely compares the current month with the previous one on a seasonally adjusted basis. The data is provided as both seasonally adjusted and non-adjusted. The detail is hidden in the published tables which we at SMU track and dissect to provide a long term perspective. Our intent is to provide a rout map for those subscribers who are dependent on this industry to “Follow the money.” This is a very broad and complex subject therefore to make this monthly write up more comprehensible we are keeping the information format as consistent as possible. In our opinion the absolute value of the dollar expenditures presented are of little interest. What we are after is the magnitude of growth or contraction of the various sectors. In the SMU analysis we consider only the non-seasonally adjusted data. We eliminate seasonal effects by comparing rolling three month expenditures year over year. CPIP data also includes the category of residential improvements which we have removed from our analysis in the rational that such expenditures are minor consumers of steel.

In the four tables included in this analysis we present the non-seasonally adjusted expenditures for the most recent month of data. Growth rates presented are all year over year and are the rate for the single months result, the rolling 3 months and the rolling 12 months. We ignore the single month year/year result in our write ups because these numbers can contain too much noise. The arrows indicate momentum. If the rolling 3 month growth rate is stronger than the rolling 12 months we define this as positive momentum and vice versa. In the text, when we refer to growth rate we are describing the rolling 3 months year over year rate. In Figures 1 through 4, the blue lines represent the rolling 12 month expenditures and the brown bars represent the rolling 3 month year over year growth rates.