Market Data

March 19, 2016

Producer Price Indexes of Sheet Steel, Aluminum, Plastic and Transportation - February 2016

Written by Peter Wright

Each month the Bureau of Labor Statistics (BLS) puts out its series of producer price indexes, for thousands of goods and materials. For an explanation of this program see the end of this piece. The latest release last week reported results through February. We run this analysis every three or four months to give readers an opportunity to become aware of any changes in the competitive position of steel against other materials and rail vs truck transportation.

The PPI data are helpful in monitoring the price direction of steel and steel products against competing materials and products. As far as we at SMU can tell from comparison with known transaction prices, these PPI are a good representation of the real world. However our observation is that the actual values of the PPIs of different products cannot be compared with one another because they are developed by different committees within the BLS. We believe that this data is useful in comparing the direction of prices in the short and medium term but not the absolute value.

The February report from the BLS read as follows; From February 2015 to February 2016, the Producer Price Index for final demand was unchanged. Over that same 12-month period, the index for final demand less foods, energy, and trade services increased 0.9 percent, the largest over-the-year increase since July 2015. The Producer Price Index for final demand goods decreased 2.7 percent for the year ending February 2016. The index for final demand energy fell 14.5 percent over that 12-month period. The index for final demand services increased 1.5 percent from February 2015 to February 2016. These data are from the Producer Price Indexes program and are not seasonally adjusted. All producer price indexes are subject to revision once, 4 months after original publication, reflecting late reports and corrections by respondents. Producer price indexes measure prices U.S. producers receive for goods, services, and construction.

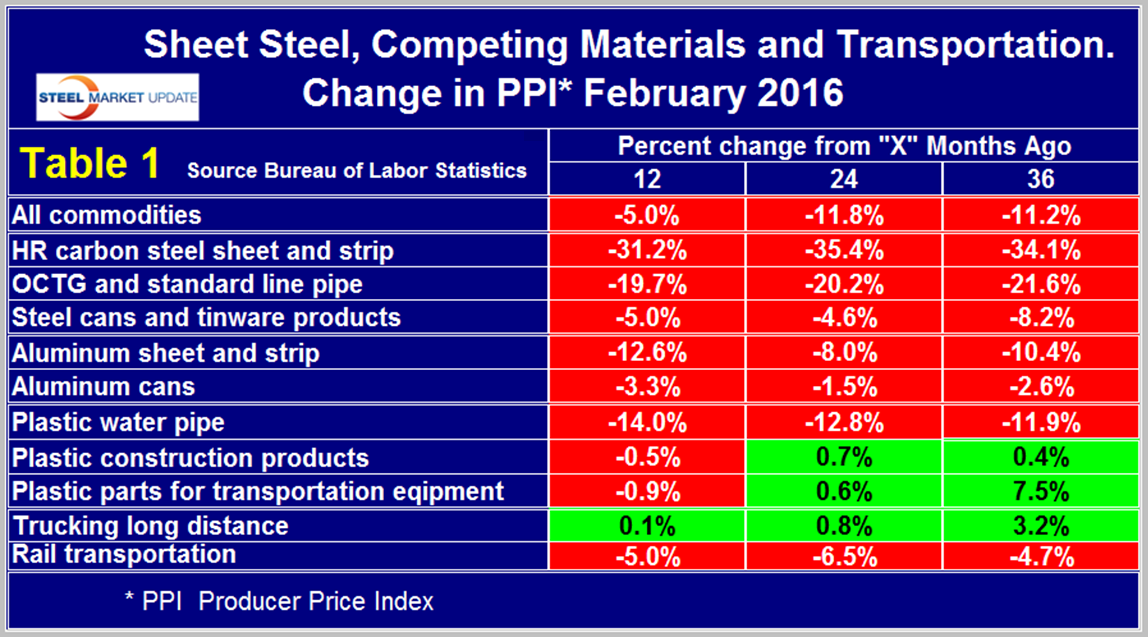

For the purpose of this report, we at SMU have extracted comparative statistics for sheet steel, aluminum and plastic products and truck and rail transportation. Table 1 is a summary of each category on a year over one, two and three year basis.

On a first macro comparison Table 1 for February has exactly the same gain/loss pattern as shown by the color codes as it did in our November update except that in the latest data the cost of truck transportation had a small increase. Our analysis of the PPI data shows that commodity prices as a whole declined by 5.0 percent in 12 months through February which was a slower rate of decline than in the 24 and 36 month comparisons. Commodity prices in general were back to where they were at the beginning of 2010. A rising $ will put downward pressure on commodity prices. It is evident from Table 1 that carbon steel sheet has declined much more than aluminum sheet which has resulted in steel cans gaining a competitive advantage over aluminum cans. In a similar vein steel pipe has declined much more than plastic pipe. AMM reported on February 5th that the collapse of steel and plastic prices has strengthened the position that each holds at opposite ends of the oil and gas supply chain. Steel dominates in most oil production and refining applications as plastic is used more often in distribution, mostly of natural gas, to end users. An analyst with Cleveland based Freedom Group Inc., told AMM that plastic made significant inroads in oil and gas pipe applications in 2009 through 2012 but since then inroads have slowed.

The prices of plastic construction products and plastic parts for transportation equipment have declined very little in the last 12 months in spite of the collapse in hydrocarbon prices.

Table 1 also shows price changes for truck and rail transportation and indicates that rail has become more competitive in all three time periods considered.

The official description from the Bureau of Labor Statistics (BLS) reads as follows: The Producer Price Index (PPI) is a family of indexes that measure the average change over time in the prices received by domestic producers of goods and services. PPIs measure price change from the perspective of the seller. This contrasts with other measures, such as the Consumer Price Index (CPI). CPIs measure price change from the purchaser’s perspective. Sellers’ and purchasers’ prices can differ due to government subsidies, sales and excise taxes, and distribution costs. More than 9,000 PPIs for individual products and groups of products are released each month. PPIs are available for the products of virtually every industry in the mining and manufacturing sectors of the U.S. economy. New PPIs are gradually being introduced for the products of industries in the construction, trade, finance, and services sectors of the economy. More than 100,000 price quotations per month are organized into three sets of PPIs: (1) Stage-of-processing indexes (2) commodity indexes, and (3) indexes for the net output of industries and their products. The stage-of processing structure organizes products by class of buyer and degree of fabrication. The commodity structure organizes products by similarity of end use or material composition. The entire output of various industries is sampled to derive price indexes for the net output of industries and their products.