Prices

January 20, 2016

SMU Price Ranges & Indices: Prices Move Higher

Written by John Packard

The domestic steel mills announced a new round of price increases earlier this month. Steel prices are responding by moving higher, at least by a portion of the second increase. We are hearing from our sources that the mills have been able to collect $40-$50 or essentially all of the first price increase by this point in time. Now we will see if the mills have enough demand and desire to move prices higher from here. At this time, it is our opinion that momentum is on the side of the domestic steel mills and we will talk about this more in the coming days (as well as potentially challenges the mills have on moving prices too high, too fast).

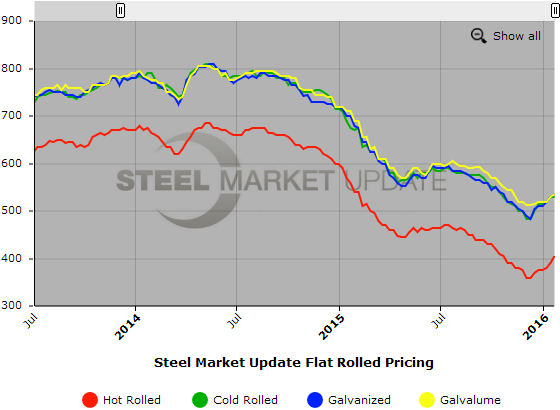

Based on the results of our flat rolled steel survey begun on Monday morning of this week here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $380-$430 per ton ($19.00/cwt- $21.50/cwt) with an average of $405 per ton ($20.25/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago while the upper end increased $20 per ton. Our overall average $15 higher over last week. SMU price momentum for hot rolled steel has prices rising over the next 30 days.

Hot Rolled Lead Times: 3-6 weeks.

Cold Rolled Coil: SMU Range is $510-$550 per ton ($25.50/cwt- $27.50/cwt) with an average of $530 per ton ($26.50/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to last week while the upper end increased $10 per ton. Our overall average is unchanged compared to one week ago. SMU price momentum for cold rolled steel is for prices to increase over the next 30 days.

Cold Rolled Lead Times: 4-8 weeks.

Galvanized Coil: SMU Base Price Range is $25.50/cwt-$28.00/cwt ($510-$560 per ton) with an average of $26.75/cwt ($535 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to one week ago while the upper end increased $20 per ton. Our overall average $5 higher over last week. Our price momentum on galvanized steel is for prices to move higher over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $570-$620 per net ton with an average of $595 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-10 weeks.

Galvalume Coil: SMU Base Price Range is $25.50/cwt-$28.00/cwt ($510-$560 per ton) with an average of $26.75/cwt ($535 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to last week while the upper end increased $20 per ton. Our overall average is $5 per ton higher than it was one week ago. Like the other flat rolled products mentioned above our price momentum for Galvalume is currently pointing towards an increase in prices over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $801-$851 per net ton with an average of $826 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-8 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.