Market Data

December 23, 2015

The Chicago Federal Reserve National Activity Index and Steel Supply

Written by Peter Wright

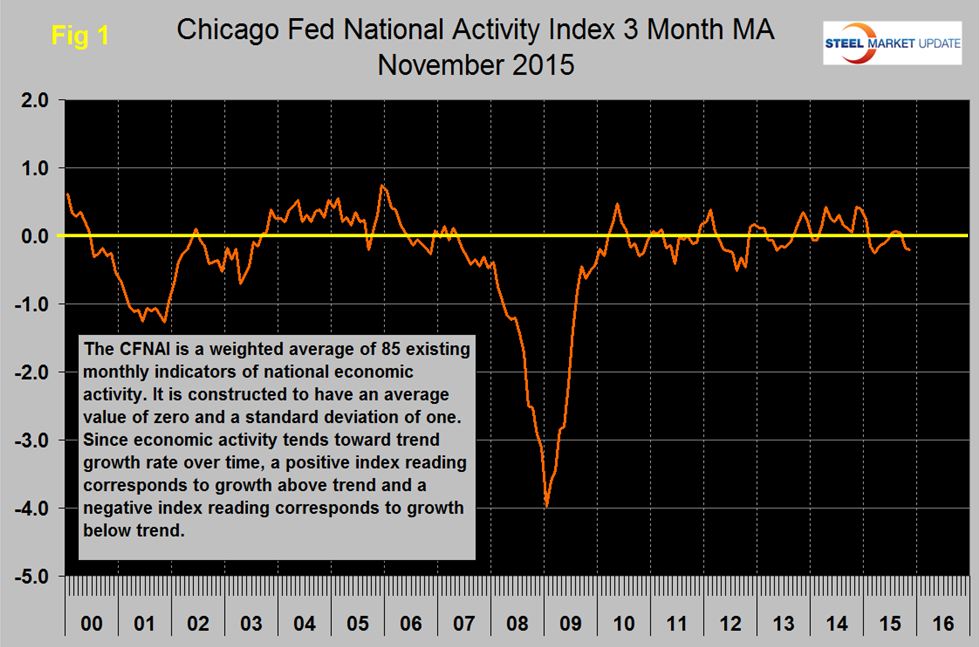

The following is the Chicago Federal Reserve statement followed by our own graphical analysis. The CFNAI is an excellent reality check for much of the economic analysis that we routinely provide in The Steel Market Update and is also a reasonably good predictor of the direction of steel demand with a six to nine month lead. For example by the time the steel market went off the cliff in September 2008, the CFNAI had been signaling an increasingly severe problem for eight months. Then in the first Q of 2009 the CFNAI was recovering as steel supply was still going south. An explanation of the Index is provided at the end of this piece.

![]() The official statement reads as follows:

The official statement reads as follows:

Index shows economic growth slowed in November

The index’s three-month moving average, CFNAI-MA3, decreased to –0.20 in November from –0.18 in October. November’s CFNAI-MA3 suggests that growth in national economic activity was somewhat below its historical trend. The economic growth reflected in this level of the CFNAI-MA3 suggests subdued inflationary pressure from economic activity over the coming year.

Thirty-seven of the 85 individual indicators made positive contributions to the CFNAI in November, while 48 made negative contributions. Thirty-nine indicators improved from October to November, while 44 indicators deteriorated and two were unchanged. Of the indicators that improved, 16 made negative contributions.

The contribution from production-related indicators to the CFNAI decreased to –0.27 in November from –0.11 in October. Industrial production declined by 0.6 percent in November after decreasing by 0.4 percent in October. Moreover, manufacturing production was unchanged in November, following an increase of 0.3 percent in the previous month.

Employment-related indicators contributed +0.05 to the CFNAI in November, down slightly from +0.08 in October. Nonfarm payrolls increased by 211,000 in November after rising by 298,000 in October, while the unemployment rate was unchanged at 5.0 percent in November.

The contribution of the personal consumption and housing category to the CFNAI edged up to –0.06 in November from –0.11 in October. Housing starts increased to 1,173,000 annualized units in November from 1,062,000 in October. In addition, housing permits moved up to 1,289,000 annualized units in November from 1,161,000 in the previous month. The sales, orders, and inventories category made a contribution of –0.02 to the CFNAI in November, up slightly from –0.03 in October.

The CFNAI was constructed using data available as of December 17, 2015. At that time, November data for 51 of the 85 indicators had been published. For all missing data, estimates were used in constructing the index. The October monthly index value was revised to –0.17 from an initial estimate of –0.04, and the September monthly index value was revised to –0.13 from last month’s estimate of –0.29. Revisions to the monthly index value can be attributed to two main factors: revisions in previously published data and differences between the estimates of previously unavailable data and subsequently published data. The revision to the October monthly index value was due primarily to the former, while the revision to the September monthly index value was due primarily to the latter.

The CFNAI has declined for four straight months through November and has declined in nine of the first eleven months of 2015 (see explanation below). Figure 1 shows the SMU analysis of the three month moving average (3MMA) through November and that the index was slightly positive each month July through September, declined to negative 0.18 in September and again to negative 0.20 in November.

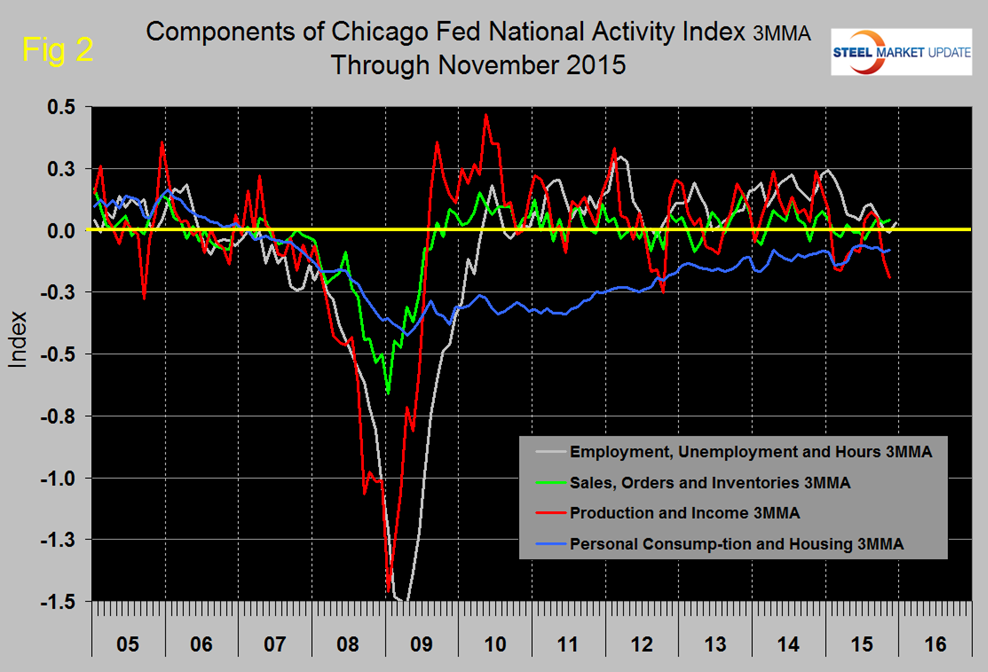

Figure 2 shows the trends of the four main subcomponents.

There was a gradual five year improvement in personal consumption and housing through mid-2015 but since then this component has lost direction. The other three sub-components continue to be erratic with a strong downward trend in employment and hours worked which doesn’t seem to jive with the Bureau of Labor Statistics data. There has been a marked drop in production and income in the last three months. If our observations here seem to be at odds with the official statement it is because we discuss only three month moving averages.

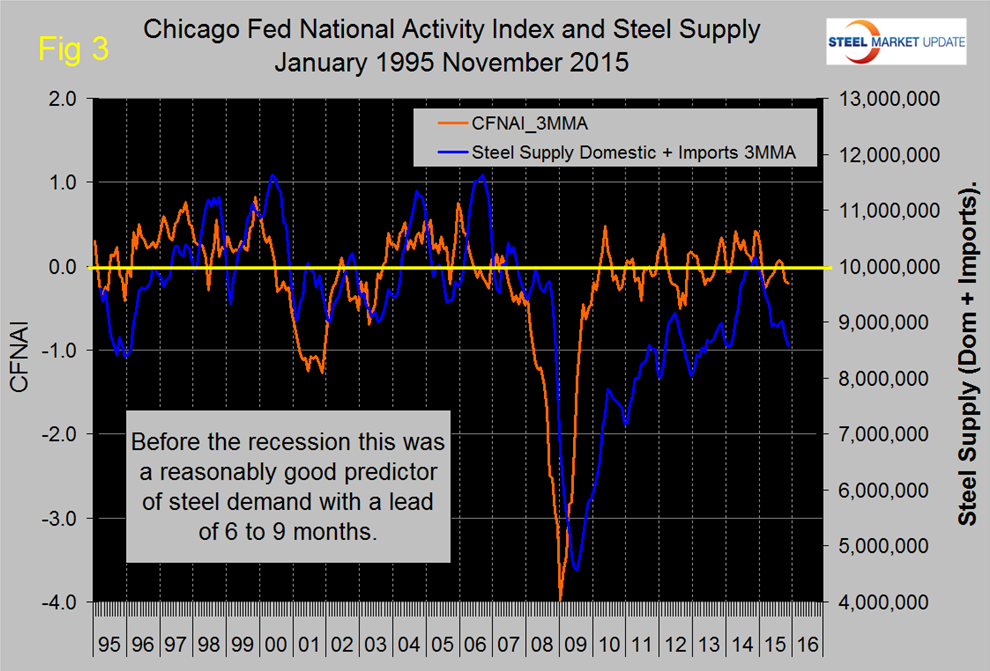

Figure 3 compares the 3MMA of steel supply with the CFNAI and shows that the index has historically been a reasonably accurate leading indicator of steel demand (apparent supply) with a lead time of six to nine months.

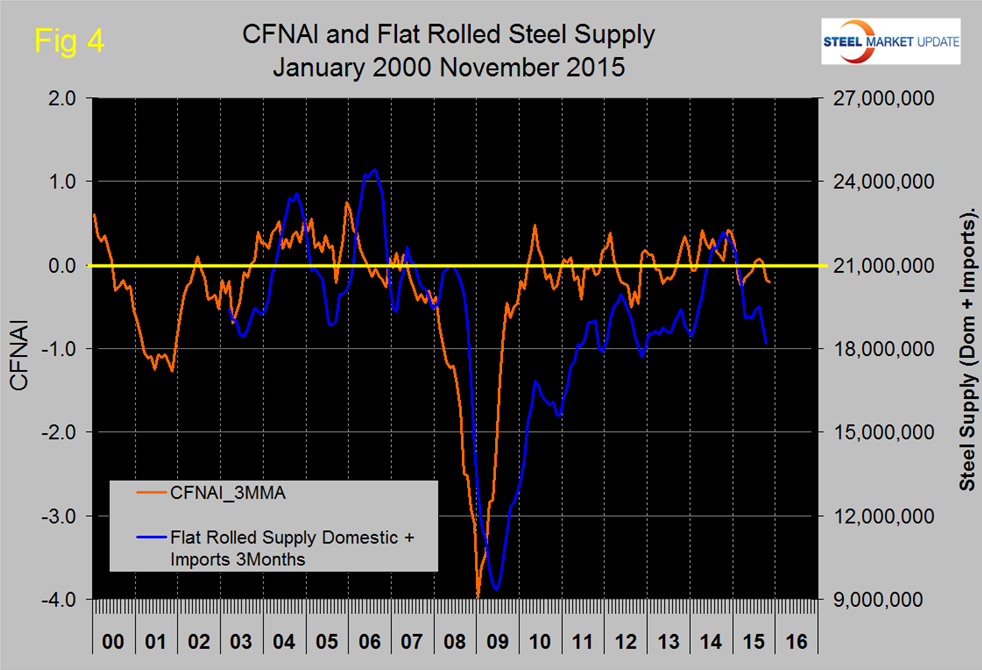

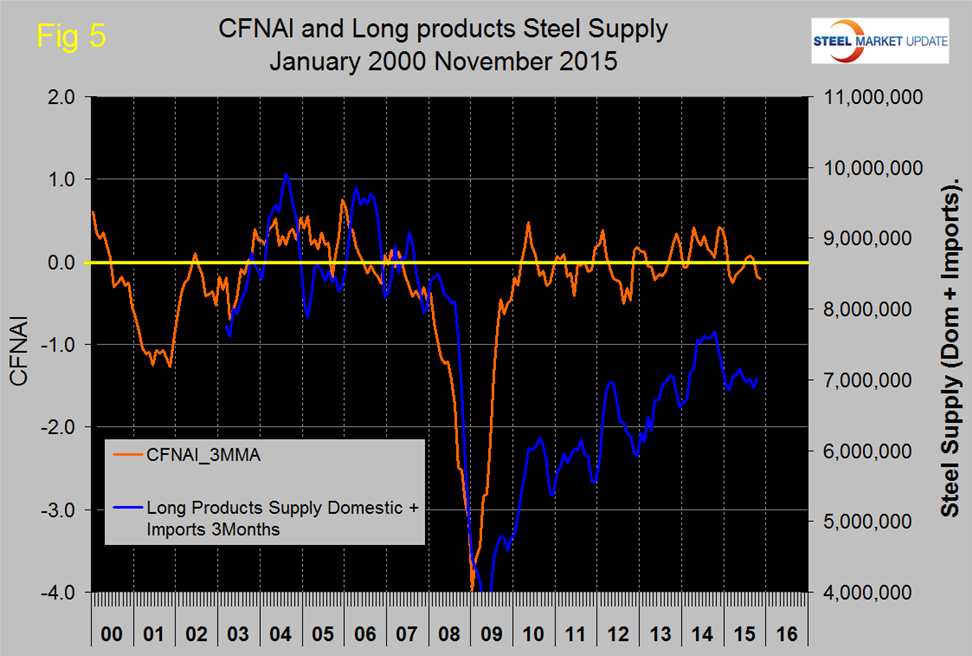

SMU monitors several benchmark indicators to evaluate whether steel consumption is where it should be based on historical patterns, this is one of them. Total steel supply closed the gap in the period mid 2009 through Q4 2014 but in the last twelve months has fallen off again probably as a result of the depressed energy sector. Figure 4 and Figure 5 show this same relationship for flat rolled and long products separately, based on a rolling three months tonnage for each.

The difference is quite dramatic and qualitatively in agreement with our analysis of steel service center shipments. Flat rolled driven mainly by manufacturing came back in line at the end of 2014 but this year has fallen off again as demand from the energy sector has collapsed. Long products driven mainly by construction is still depressed and since the recession has not come anywhere near where this benchmark predicts. Based on the historical lead of the CFNAI it no longer looks as though total steel demand will pick up through Q1 2016. Note; steel supply shown is only through October as that is the latest data available.

Explanation: The index is a weighted average of 85 indicators of national economic activity drawn from four broad categories of data: 1) production and income; 2) employment, unemployment, and hours; 3) personal consumption and housing; and 4) sales, orders, and inventories. A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth. When the CFNAI-MA3 (three month moving average) value moves below –0.70 following a period of economic expansion, there is an increasing likelihood that a recession has begun. Conversely, when the CFNAI-MA3 value moves above –0.70 following a period of economic contraction, there is an increasing likelihood that a recession has ended. When the CFNAI-MA3 value moves above /+0.70 more than two years into an economic expansion, there is an increasing likelihood that a period of sustained increasing inflation has begun.