Prices

June 2, 2015

SMU Price Ranges & Indices:

Written by John Packard

When speaking to buyers and sellers of flat rolled steel this week, one theme became abundantly clear: everyone is waiting for trade cases and, second, where scrap prices will end up for the month of June. Both are expected to support a further tightening of steel prices. Scrap is expected to rise anywhere from $10 to as much as $30 per gross ton depending on region and product. Trade case rumors continue to persist with one service center advising SMU this evening that he was “99.9%” sure that coated trade cases will be filed on Wednesday of this week. We will wait to see what tomorrow brings.

We have heard from other sources that “Thursday” will be the day. The sources are coming from different segments of the industry so perhaps there is an element of truth to the rumors. Any announcement would tighten up flat rolled prices and set the stage from new increase announcements.

However, we are jumping the gun so, here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Don’t let the adjustments up a few dollars or down a few dollars affect the thinking on market direction. We are in a short term holding pattern as the market waits for what will propel prices higher from here. SMU is still convinced that Momentum is for prices to move higher over the next 30 to 60 days.

Hot Rolled Coil: SMU Range is $440-$480 per net ton ($22.00/cwt- $24.00/cwt) with an average of $460 per ton ($23.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to last week while the upper end of our range was unchanged. Our average is now $5 per ton lower compared to one week ago. SMU price momentum for hot rolled steel is for prices to trend slowly higher over the next 30 to 60 days.

Hot Rolled Lead Times: 3-6 weeks.

Cold Rolled Coil: SMU Range is $560-$600 per net ton ($28.00/cwt- $30.00/cwt) with an average of $580 per ton ($29.00/cwt) FOB mill, east of the Rockies. Both the upper and lower end of our range remained the same compared to one week ago. Our average is unchanged compared to last week. We continue to believe that price momentum on cold rolled steel is for prices to slowly move higher over the next 30 to 60 days. Any trade case filings would most likely escalate higher prices and longer lead times (stay tuned).

Cold Rolled Lead Times: 4-7 weeks.

Galvanized Coil: SMU Base Price Range is $27.50/cwt-$29.50/cwt ($550-$590 per net ton) with an average of $28.50/cwt ($570 per ton) FOB mill, east of the Rockies. Both the upper and lower end of our range remained the same compared to last week. Our average is unchanged compared to one week ago SMU anticipates galvanized prices to move slowly higher over the next 30 to 60 days. Any trade case will have an impact on galvanized lead times and tighten prices (plus embolden the mills to move GI prices higher).

Galvanized .060” G90 Benchmark: SMU Range is $619-$659 per net ton with an average of $639 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-8 weeks.

Galvalume Coil: SMU Base Price Range is $27.50/cwt-30.00/cwt ($550-$600 per net ton) with an average of $28.75/cwt ($575 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to one week ago while the upper end of our range was unchanged. Our average is now $5 less than last week. Our expectation is for Galvalume prices to slowly move higher over the next 30 to 60 days. The question is will the domestic mills include Galvalume in any coated trade case filing. With foreign steel now controlling more than 50 percent of the domestic market we expect that AZ dumping suits will be filed. Any filing would affect both lead times and pricing.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $841-$891 per net ton with an average of $866 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4-6 weeks.

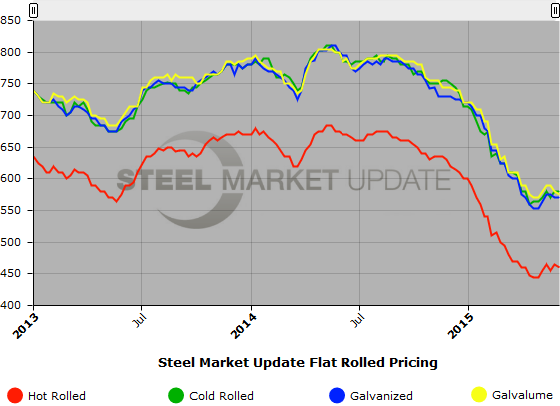

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website. You can do this by clicking here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.