Market Data

April 2, 2015

The ISM Manufacturing Index Retreated Again in March

Written by Peter Wright

The Institute of Supply Management released their March report on April 1st. An explanation of the ISM index is given at the end of this piece. After the October surprise on the upside, the index slid back to 55.1 in December to 53.5 in January, to 52.9 in February and to 51.5 in March.

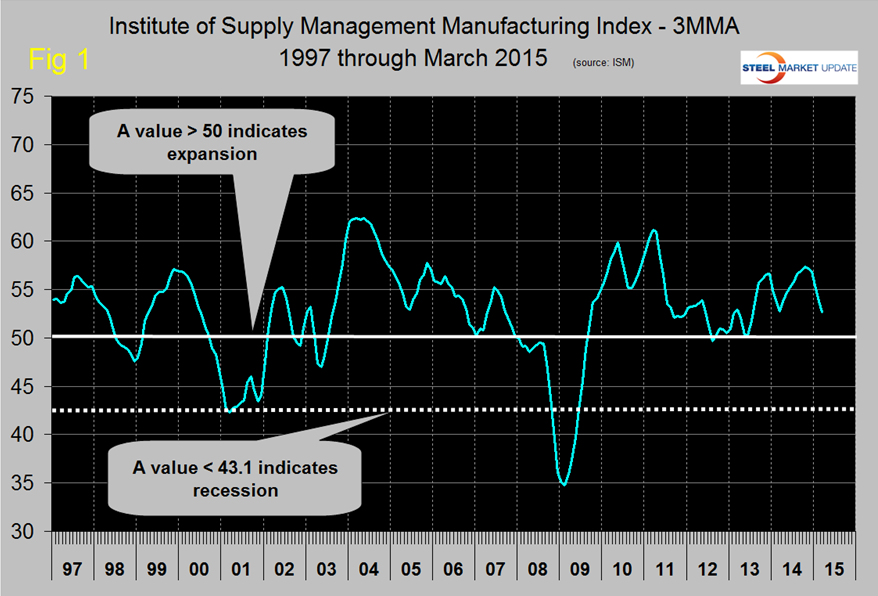

Any number >50 indicates expansion but clearly a slowdown is occurring in this index. The three month moving average has declined for five straight months and now stands at 52.63, which is 2.57 points below the 15 month average since January last year. This was the 30th straight month for which the 3MMA indicated growth (Figure 1).

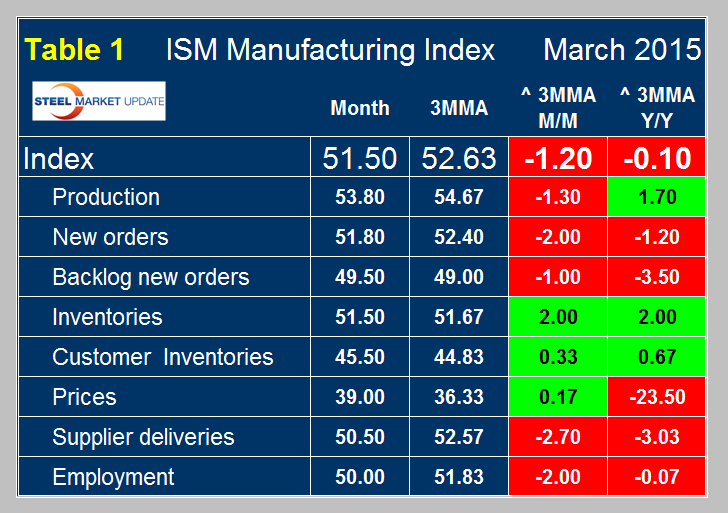

Table 1 shows the break down for March by sub component with the monthly result, the 3MMA, the growth of the 3MMA month over month (m/m) and year over year (y/y) for each. The table shows that the 3MMA y/y growth was negative 0.1 which was the first negative growth y/y since March last year. The good news is that there are more green cells in Table 1 than when we last published. On a m/m basis customer inventories and prices both improved. The price component in March was down by 23.5 points from this time last year but eked out a small gain of 0.17 points m/m. Bad news is that employment has negative growth both on a m/m and y/y basis.

By this measure manufacturing slowed in the first quarter. The industrial production index for March won’t be released until mid-month but the February data did suggest a slowdown in growth. We will reserve judgment on whether the expansion of manufacturing is really slowing until the March IP data is released. Please note by no measure are we seeing a contraction, just a slower rate of growth. Some possible causes of a slowdown such as the disruption at the West Coast ports will fade but the appreciating US dollar is bound to be a headwind for the immediate future.

The official news release reads as follows:

New Orders, Production and Inventories Growing, Employment Unchanged, Supplier Deliveries Slowing

(Tempe, Arizona) — Economic activity in the manufacturing sector expanded in March for the 27th consecutive month, and the overall economy grew for the 70th consecutive month, say the nation’s supply executives in the latest Manufacturing ISM Report On Business.

The report was issued today by Bradley J. Holcomb, CPSM, CPSD, chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee. “The March PMI registered 51.5 percent, a decrease of 1.4 percentage points from February’s reading of 52.9 percent. The New Orders Index registered 51.8 percent, a decrease of 0.7 percentage point from the reading of 52.5 percent in February. The Production Index registered 53.8 percent, 0.1 percentage point above the February reading of 53.7 percent. The Employment Index registered 50 percent, 1.4 percentage points below the February reading of 51.4 percent, reflecting unchanged employment levels from February. Inventories of raw materials registered 51.5 percent, a decrease of 1 percentage point from the February reading of 52.5 percent. The Prices Index registered 39 percent, 4 percentage points above the February reading of 35 percent, indicating lower raw materials prices for the fifth consecutive month. Comments from the panel refer to continuing challenges from the West Coast port issue, lower oil prices having both positive and negative impacts depending upon the industry, residual effects of the harsh winter, higher costs of healthcare premiums, and challenges associated with the stronger dollar on international business.”

Of the 18 manufacturing industries, 10 are reporting growth in March in the following order: Paper Products; Wood Products; Transportation Equipment; Fabricated Metal Products; Nonmetallic Mineral Products; Machinery; Chemical Products; Primary Metals; Food, Beverage & Tobacco Products; and Computer & Electronic Products. The seven industries reporting contraction in March — listed in order — are: Apparel, Leather & Allied Products; Textile Mills; Petroleum & Coal Products; Electrical Equipment, Appliances & Components; Miscellaneous Manufacturing; Plastics & Rubber Products; and Furniture & Related Products.

What respondents are saying:

– “Falling energies have helped on the cost side while sales are getting a boost through improvements in consumer disposable income.” (Food, Beverage & Tobacco Products)

– “Our business is still strong and on projection. Dollar strength is challenging for our international business.” (Fabricated Metal Products)

– “Business is still extremely strong.” (Transportation Equipment)

– “Oil prices impacting drilling and project activity. Pursuing cost reductions from suppliers for a wide variety of goods and services.” (Petroleum & Coal Products)

– “Business really starting to slow down. Oil pricing is having a major effect on energy markets.” (Computer & Electronic Products)

– “Steady Q1 demand but somewhat interrupted by weather.” (Primary Metals)

– “Operating costs are higher due to increases in healthcare premiums.” (Miscellaneous Manufacturing)

– “March business is improving over Jan-Feb, thawing out of this crazy winter.” (Paper Products)

– “Dealing with ongoing delivery issues associated with congestion at the U.S. West Coast and Vancouver ports.” (Machinery)

– “Congestion at the West Coast ports delaying incoming products.” (Textile Mills)

Explanation: The Manufacturing ISM Report On Business is published monthly by the Institute for Supply Management, the first supply institute in the world. Founded in 1915, ISM exists to lead and serve the supply management profession and is a highly influential and respected association in the global marketplace. ISM’s mission is to enhance the value and performance of procurement and supply chain management practitioners and their organizations worldwide. This report has been issued by the association since 1931, except for a four-year interruption during World War II. The report is based on data compiled from purchasing and supply executives nationwide. Membership of the Manufacturing Business Survey Committee is diversified by NAICS, based on each industry’s contribution to gross domestic product (GDP). The PMI is a diffusion index. Diffusion indexes have the properties of leading indicators and are convenient summary measures showing the prevailing direction of change and the scope of change. A PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining. A PMI in excess of 42.2 percent, over a period of time, indicates that the overall economy, or gross domestic product (GDP), is generally expanding; below 42.2 percent, it is generally declining. The distance from 50 percent or 42.2 percent is indicative of the strength of the expansion or decline. With some of the indicators within this report, ISM has indicated the departure point between expansion and decline of comparable government series, as determined by regression analysis.