Analysis

December 16, 2014

Housing Starts, Permits and Builder Confidence

Written by Peter Wright

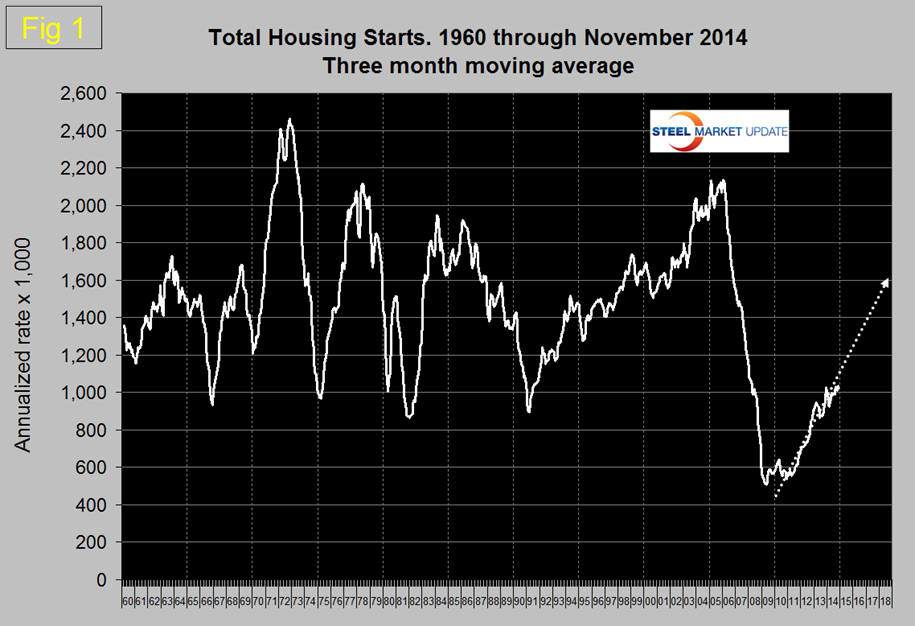

Starts in November declined to an annual rate 1,028,000, the same as the number for September but down from 1,045,000 in October. The three month moving average, (3MMA) rose to 1,034,000, (Figure 1). This was the third consecutive month that the 3MMA of starts exceeded a million units. The year over year growth rate of the 3MMA of total starts in October was 6.8 percent. Total starts are still on track to reach 1.6 million by the end of 2018.

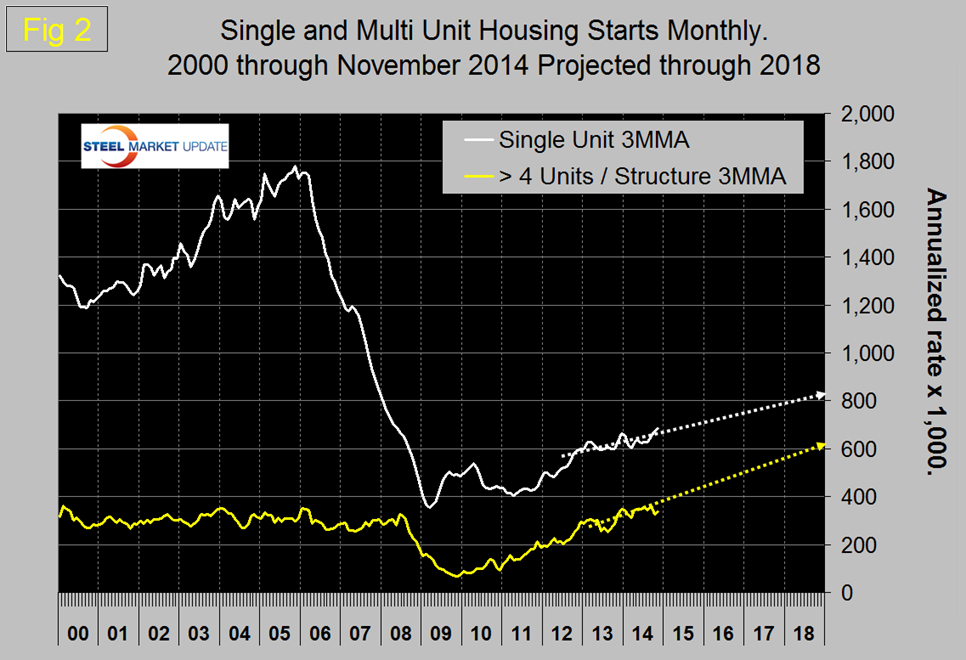

Multifamily starts are now beyond the pre-recession high of January 2006 but single family are still 62.9 percent below the level enjoyed at that time, (Figure 2).

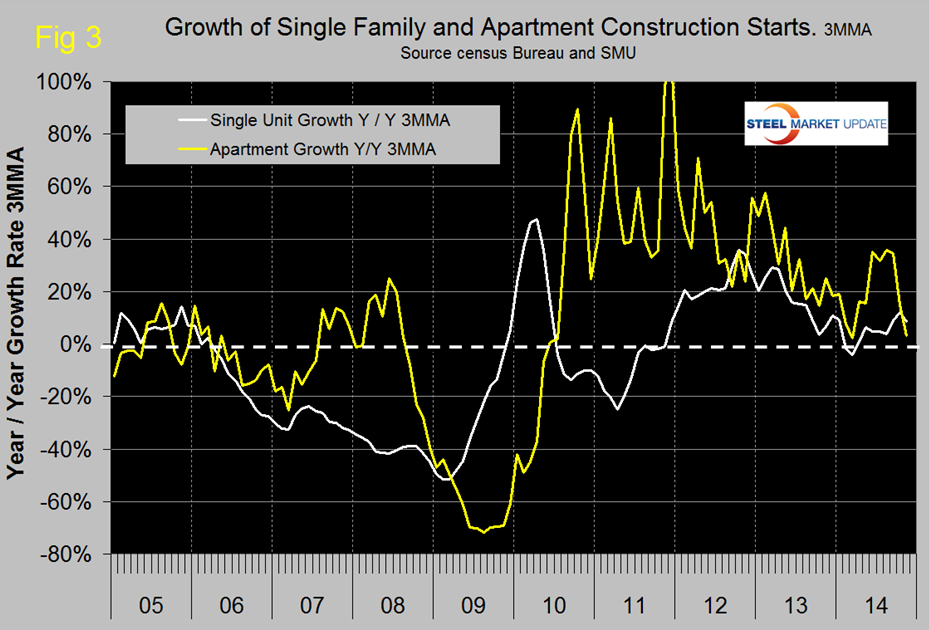

In October the growth rate of multifamily starts slowed from the mid-30s which had prevailed since May to 14.9 percent, then in November slowed again to 3.1 percent. Single family which had the first double digit gain of the year in October at 12.1 percent slowed to 8.5 percent in November, (Figure 3). Both on a 3MMA year over year basis.

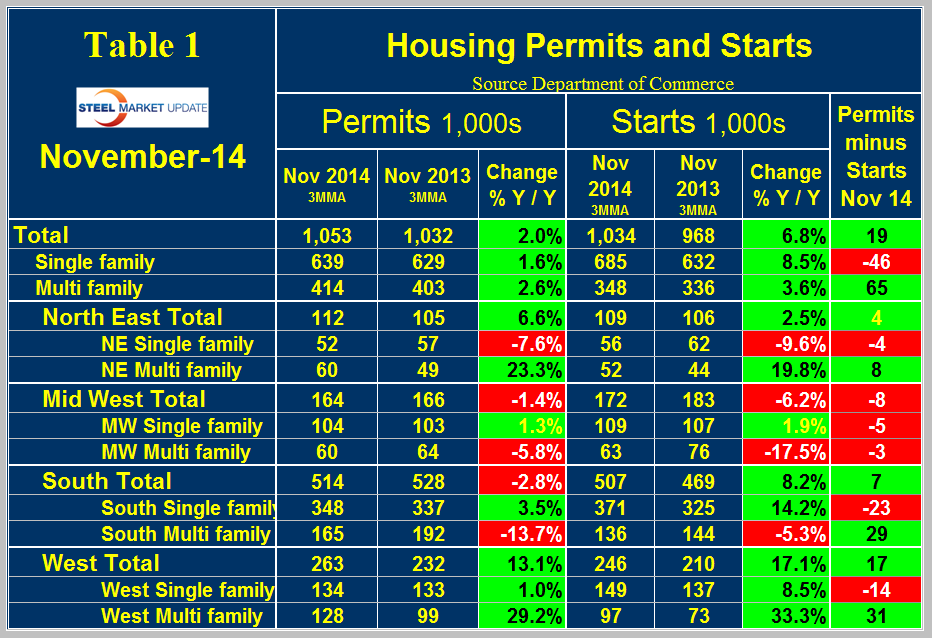

Permit data is useful to evaluate where future starts are headed. If permits exceed starts then we anticipate an acceleration and vice versa. Table 1 shows that total permits did exceeded starts by 19,000 in November on a 3MMA basis.

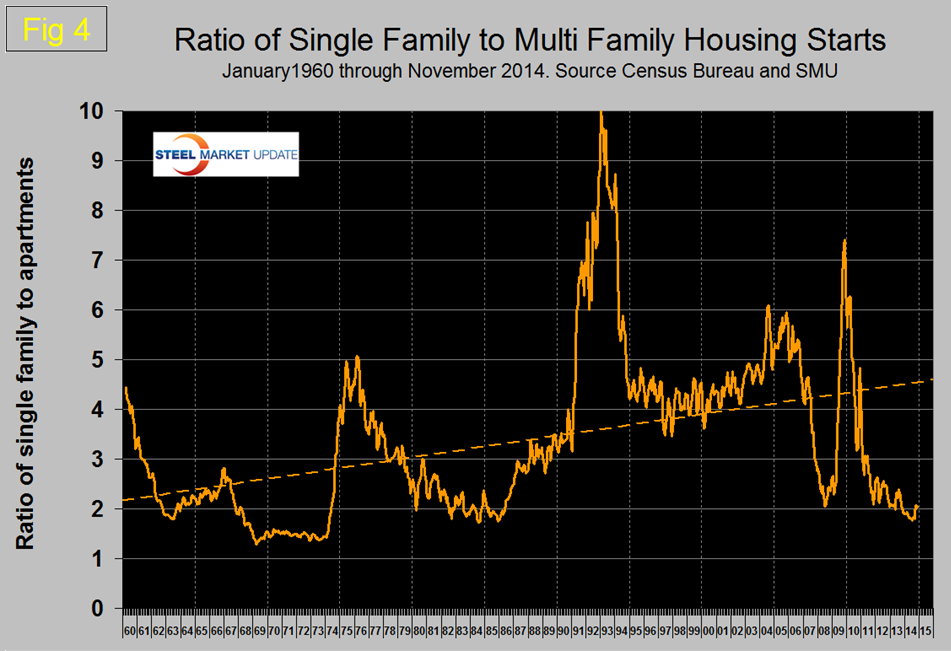

However the situation continues to be dramatically different for single and multi-family units. Single family permits were 46,000 less than starts and multi-family permits were 65,000 more than starts. This signals a future acceleration in multi-family and a deceleration in single family. The ratio of the two sectors is shown in Figure 4 and demonstrates that single family compared to multifamily has improved slightly but single family homes continue to be less desirable than at any time in the last 30 years. Based on permit data this trend will not change any time soon.

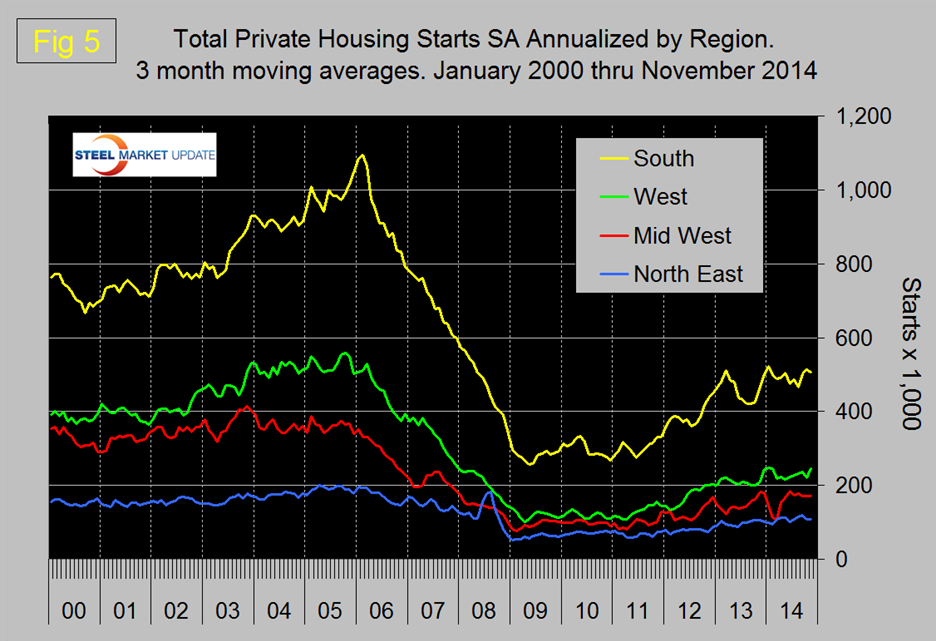

The situation in the four regions reported in the Census Bureau report were not synchronous in November. The West was the only region to have positive growth in total starts on a 3MMA basis and most of that growth was in multi-family. The Mid West and South actually had a year over year decline in both multi-family permits and starts. The NE still has strong growth in multifamily but single family construction is slowing. Figure 5 shows the regional situation for total residential starts since January 2000.

Student loan debt exceeded $1.3 trillion in Q3 2014 for the first time, this must be impacting the young person’s view of other debt obligations and so presumably is the view that housing is not necessarily the great investment that it was once thought to be. In addition uncertainty in the job market makes mobility desirable and promotes the idea of rent in preference to purchase. To attempt to counter these trends Fannie Mae and Freddie Mac have introduced a new program for first time buyers that requires only a 3 percent down payment down from what has become the traditional 20 percent level since the subprime debacle. First time buyers normally account for 40 percent of new home sales. In this case, first time is defined as not having held a mortgage for three years.

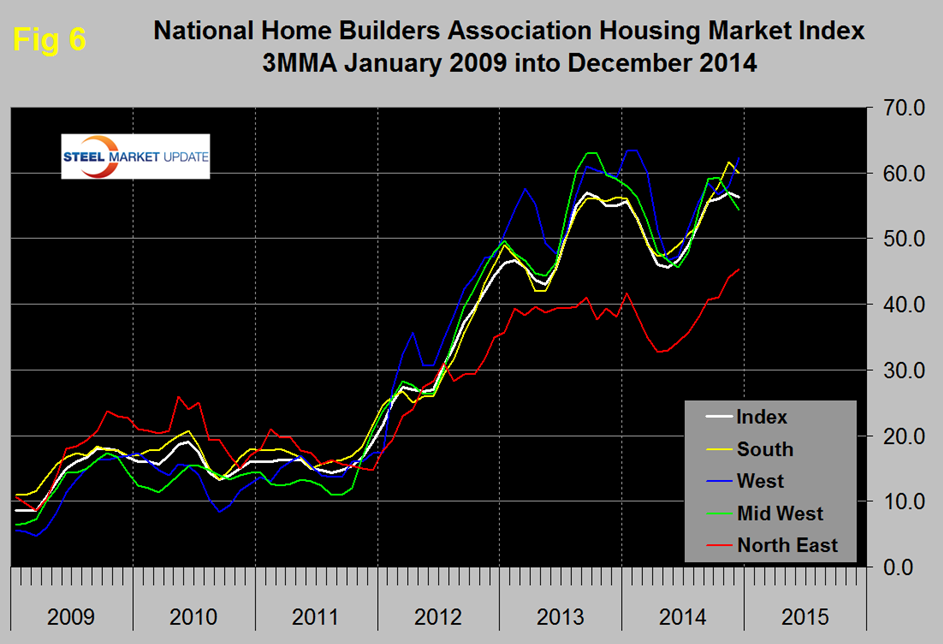

The National Association of Home Builders, (NAHB) confidence report was released on Monday, (Figure 6). Any value above 50 indicates an overall positive business confidence. The index declined by one point to 57 in December and the 3MMA declined to 56.3, still the second highest reading since September last year. The composite index, signals that homebuilders are generally positive in their views of the market.

The official release from the NAHB read as follows:

Builder Confidence Drops One Point in December

Following a four-point uptick last month, builder confidence in the market for newly built single-family homes fell one point in December to a level of 57 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today.

“Members in many markets across the country have seen their businesses improve over the course of the year, and we expect builders to remain confident in 2015,” said NAHB Chairman Kevin Kelly, a home builder and developer from Wilmington, Del.

“After a sluggish start to 2014, the HMI has stabilized in the mid-to-high 50s index level trend for the past six months, which is consistent with our assessment that we are in a slow march back to normal,” said NAHB Chief Economist David Crowe. “As we head into 2015, the housing market should continue to recover at a steady, gradual pace.”

Derived from a monthly survey that NAHB has been conducting for 30 years, the NAHB/Wells Fargo Housing Market Index gauges builder perceptions of current single-family home sales and sales expectations for the next six months as “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as “high to very high,” “average” or “low to very low.” Scores from each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

Two of the three HMI components posted slight losses in December. The index gauging current sales conditions fell one point to 61, while the index measuring expectations for future sales dropped a single point to 65 and the index gauging traffic of prospective buyers held steady at 45.

Looking at the three-month moving averages for regional HMI scores, the West rose by four points to 62 and the Northeast edged up one point to 45, while the Midwest registered a three-point loss to 54 and the South dropped two points to 60.

Editor’s Note: The NAHB/Wells Fargo Housing Market Index is strictly the product of NAHB Economics, and is not seen or influenced by any outside party prior to being released to the public. HMI tables can be found here. More information on housing statistics is also available at www.HousingEconomics.com.

SMU Comment: Even though the steel content of housing is only a small proportion of total steel consumption, housing is a leading indicator of many construction sectors such as non-residential and sub sectors of infrastructure and has a large multiplier effect in the economy as a whole. To the extent that readers businesses are influenced by the relative size of the two housing sectors they should plan for further continued growth of apartment construction and a single family sector that continues to struggle.