Market Data

August 5, 2014

Bank Lending Practices in July 2014

Written by Peter Wright

The July 2014 Senior Loan Officer Opinion Survey on Bank Lending Practices addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months. This summary is based on the responses from 75 domestic banks and 23 U.S. branches and agencies of foreign banks. Below is an abridged version of the Federal Reserve report, followed by Steel Market Update comments and graphics.

The July survey results showed a continued easing of lending standards and terms for many types of loan categories amid a broad-based pickup in loan demand. Domestic banks generally continued to ease their lending standards and various terms for commercial and industrial (C&I) loans. In contrast, foreign banks reported little change in standards and in most of the surveyed terms for C&I loans on net. Domestic respondents, meanwhile, also reported having eased standards on most types of commercial real estate (CRE) loans on balance. Although many banks reported having eased standards for prime residential real estate (RRE) loans, respondents generally indicated little change in standards and terms for other types of loans to households. However, a few large banks had eased standards, increased credit limits, and reduced the minimum required credit score for credit card loans. Banks also reported having experienced stronger demand over the past three months, on net, for many more loan categories than on the April survey.

Questions on Commercial and Industrial Lending: As has been the case in each of the past three surveys, a small percentage of domestic respondents reported having eased standards on C&I loans, both to large and middle‐market firms and to small firms, over the past three months. In contrast, moderate to large fractions of banks reported having eased various price and non-price terms on C&I loans on net. Of the terms included in the survey, banks continued to report the most widespread easing on spreads of C&I loan rates over banks’ costs of funds. In addition, for all firm sizes, a significant fraction of banks reported having reduced the cost of credit lines and decreased the use of interest rate floors on balance. Although a more moderate fraction indicated having eased loan covenants, close to one-third of the large banks in the sample reported having done so for loans extended to large and middle-market firms over the past three months. Most domestic respondents that reported having eased either standards or terms on

C&I loans over the past three months continued to cite more-aggressive competition from other banks or nonbank lenders as an important reason for having done so. Smaller numbers of banks also attributed their easing to a more favorable or less uncertain economic outlook or to an increased tolerance for risk. On the demand side, a significant fraction of banks reported having experienced stronger demand for C&I loans from firms of all sizes on balance. To explain the reported increase in loan demand, banks cited a wide range of customers’ financing needs, particularly those related to investment in plant or equipment, accounts receivable, inventories, or mergers or acquisitions.

Questions on Commercial Real Estate Lending: A modest net fraction of domestic respondents reported that they had eased standards on construction and land development loans and loans secured by nonfarm nonresidential properties over the past three months. However, respondents indicated that standards for loans secured by multifamily residential properties were unchanged on net. For all three types of CRE loans, reports of stronger demand continued to outnumber reports of weaker demand. The survey asked respondents separately about their standards for, and demand from, large and middle market firms, which are generally defined as firms with annual sales of $50 million or more, and small firms, those with annual sales of less than $50 million. Large banks are defined as those with total domestic assets of $20 billion or more as of March 31, 2014.

Questions on Residential Real Estate Lending: A moderate net fraction of domestic banks reported having eased their standards on prime residential mortgages, on net, while most indicated that standards on nontraditional mortgages and home equity lines of credit (HELOCs) were relatively little changed. Banks reported having experienced stronger demand, on balance, for prime residential mortgages for the first time since a year ago, and for HELOCs for the first time since the October 2013 survey.

Questions on Consumer Lending: A modest net fraction of domestic respondents indicated that they were more willing to make consumer installment loans relative to three months ago. Most banks, however, reported that standards and the surveyed terms on various types of consumer loans were little changed. A few large banks reported having eased lending standards, increased credit limits, and lowered minimum required credit scores on credit card loans. Meanwhile, moderate fractions of banks reported having experienced stronger demand for each of the three types of consumer loans in the survey—credit card loans, auto loans, and other consumer loans. Only a few respondents reported that demand had weakened for any of these types of loans.

There is a huge amount of valuable data in this report which can be accessed here by those readers who wish to dig deeper.

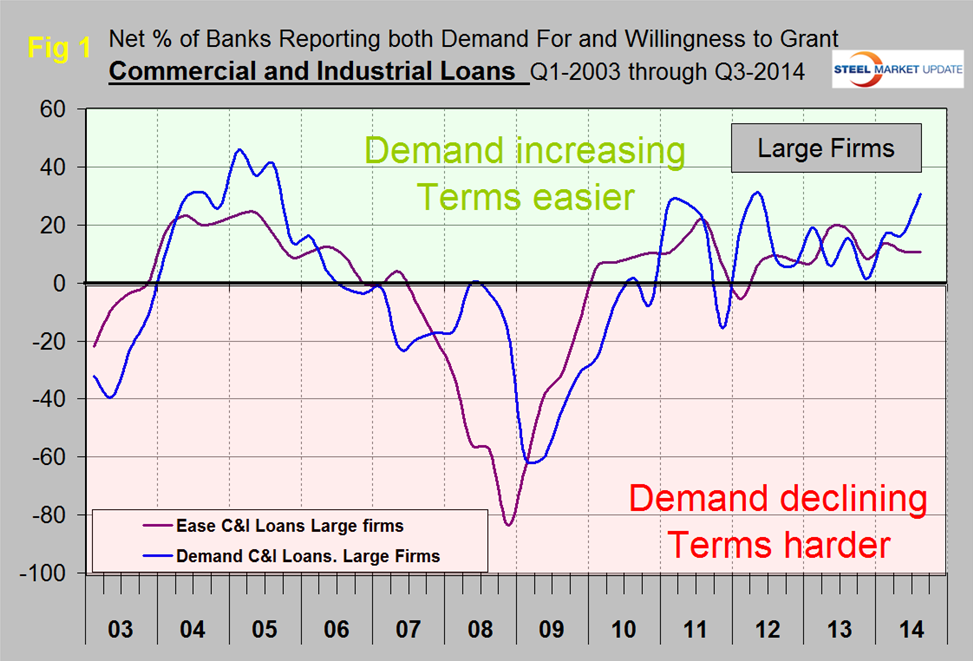

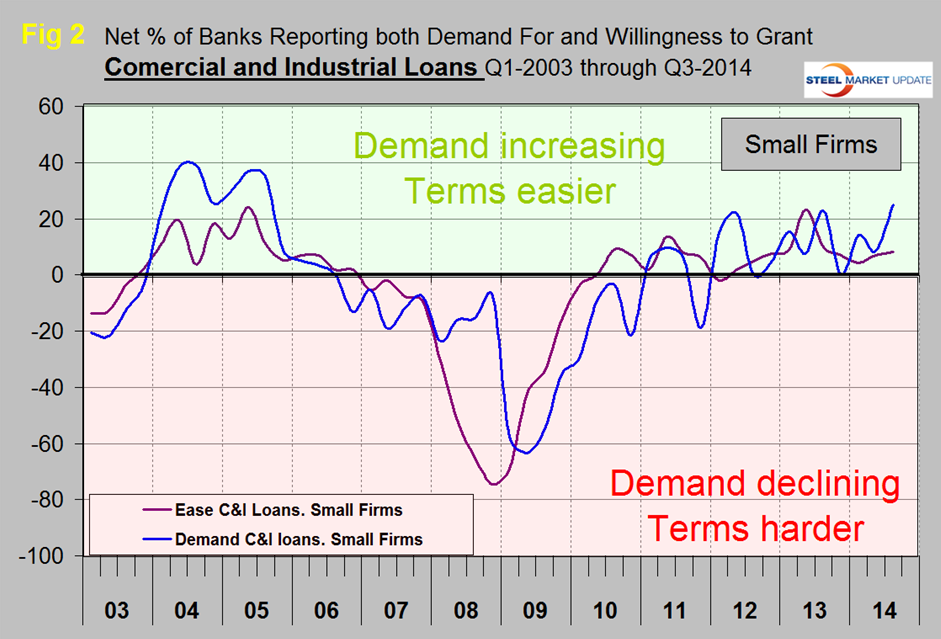

At Steel Market Update we extract and graph the major elements in the survey. Regarding loans to businesses, the July survey indicated that demand for commercial and industrial (C&I) loans from both large firms (>$50MM revenue) and small firms (<$50MM revenue) increased. Banks kept lending standards to both large and small firms little changed with a net 10.7 percent reporting easing to large firms and 8.3 percent easing to small firms, (Figure 1 and Figure 2).

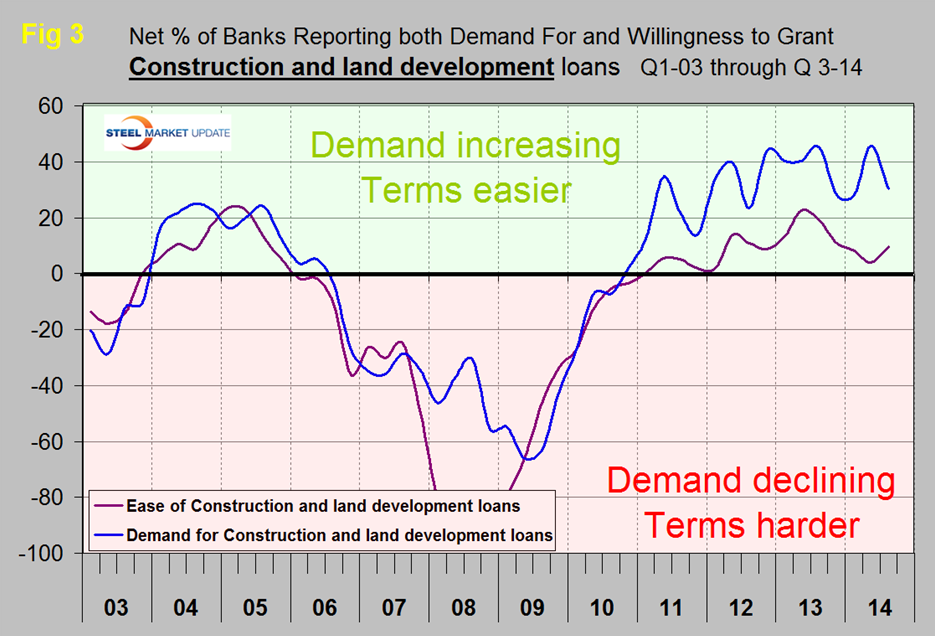

What this means, for example, is that the number of banks reporting an easing of standards to large firms was 10.7 percent higher than the proportion reporting a tightening of standards. A majority of banks are reporting a reduction in demand for construction and land development loans but the demand level is comfortably within the range that has existed since mid-2011. Lending standards eased slightly for this segment after tightening for a four quarters, (Figure 3).

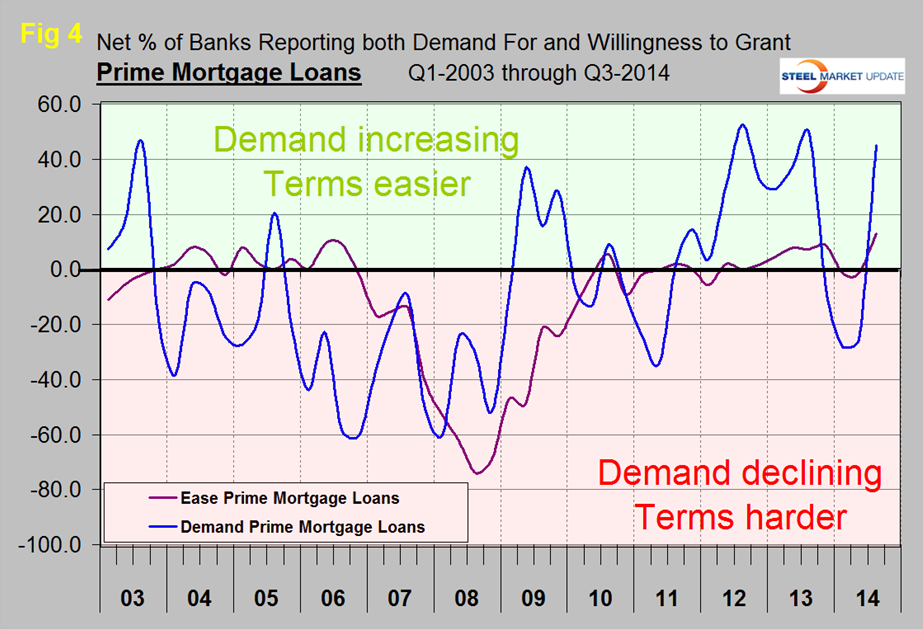

The really good news in this report is that demand for prime real-estate mortgages surged from 25.8 percent of respondents reporting reduced demand in Q2 to 45.1 percent reporting increased demand in Q3. This is a dramatic turnaround and puts demand back where it was in the period mid-2012 to mid-2013. In addition banks relaxed lending standards on balance with a net 13 percent of respondents reporting easing, (Figure 4).

The implications of this report are good for steel people and support our overall analysis of the market. Banks are relaxing standards for both industrial and construction loans and, most importantly, this report signals an improvement in the housing market which will stimulate steel demand for a wide range of products.