Market Data

May 9, 2014

Consumer Income and Debt

Written by Peter Wright

If we start with the premise that the consumer is almost 70 percent of GDP and that steel consumption is closely correlated with GDP, then consumer behavior and in particular debt is very relevant to our future businesses. Consumer spending is driven by income and both the perception of current debt and willingness to take on more. The Federal Reserve reports of personal income and credit outstanding are important pieces of the jigsaw puzzle of steel demand, past present and future.

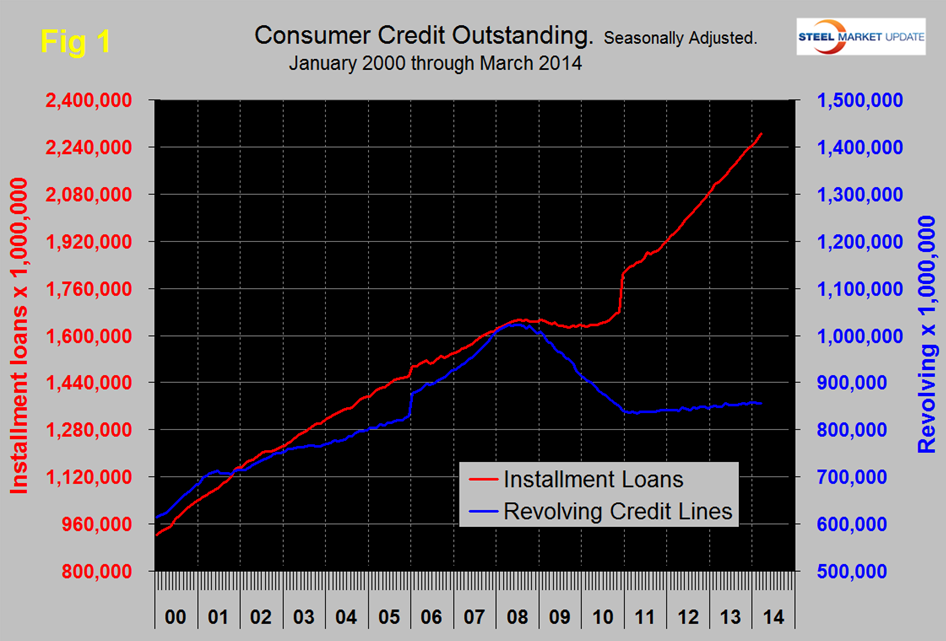

The change in the mix of consumer debt between installment (big ticket items) and revolving (credit cards) since the recession has been remarkable. In the 24 months through March, installment loans have grown by 11.3 percent and revolving loans by only 1.9 percent, (Figure 1). Consumers have clearly learned their lesson regarding the predatory nature of credit card lending and this sector has barely expanded in over three years. Unfortunately, most of the growth in the installment sector has been for student loans.

On Thursday the Armada Executive Intelligence Brief reported as follows: “Credit grew at a 5.75 percent annualized rate in the first quarter (and was accelerating at a 6.75 percent rate in March). That rate of growth is relatively consistent with what we have seen over the past decade but, it could be where the loans are building that is of most interest. Student loans were listed at $1.25 trillion at the end of March. Motor vehicle loans were $890.5 billion at the end of the same period.”

The structure of the increasing debt level is not of much help to steel providers in terms of increased consumption and it appears to us at SMU that the student loan situation is already at an unsustainable level and could precipitate the next taxpayer bailout and financial crisis.

Credit forecast.com reported as follows on April 21st – “Total U.S. household borrowing accelerated slightly to year-over-year growth of 3.2 percent in March from 3.1 percent in February. Outstanding household debt retreated $9 billion to $11.27 trillion in March, but is up $351 billion from a year earlier. Mortgage and auto loan balances increased, but balances on all other loan segments declined on seasonal factors including tax refunds. Foreclosure inventory cleansing is slowing. Mortgage refinancing dipped in March as potential homebuyers continued adjusting to hikes in mortgage rates. The total delinquency rate by volume declined sharply from 4.3 percent to 4 percent. The total annualized dollar write-off rate declined from 1.3 percent to 1.2 percent.”

To put the $11.27 trillion into perspective, it is over 70 percent of total US GDP. To our mind this is a very scary number which is why we track it and report here in the SMU each quarter.

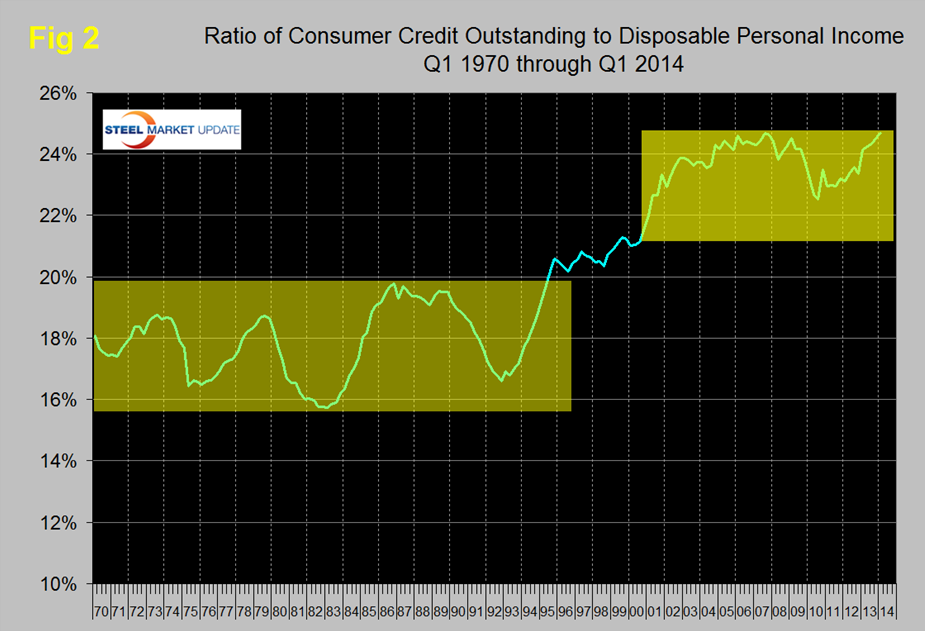

In the mid-2000s, about 2 percent of GDP was created by consumer borrowing using both credit cards and their home equity as a piggy bank. This boosted consumer demand and steel consumption. The ratio of consumer debt to personal disposable income rose from its long term range of 16 to 20 percent to over 24 percent, (Figure 2). This is only installment and revolving loans and does not include home mortgages. This ratio declined after the recession but is now at an all-time high having just passed the previous peak of Q3 2007.

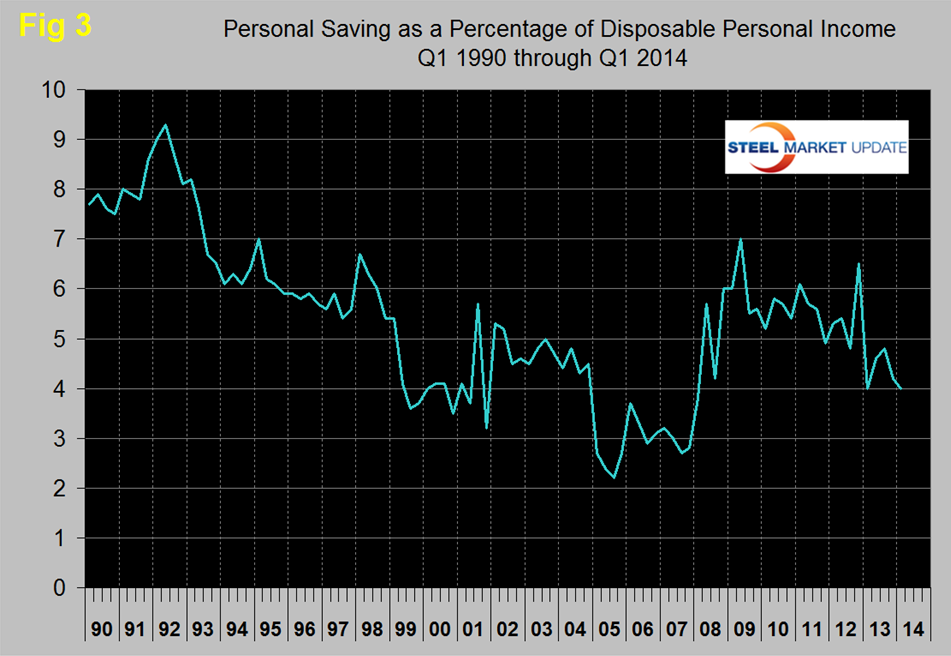

Consumer savings as a percentage of disposable personal income in Q1 2014 were at the lowest level since before the recession, (Figure 3).

The quarterly report from the Bureau of Economic Analysis on personal income and its disposition is one of the indicators that we track in our Key Market Indicators analysis which is published at the end of each month for our premium subscribers. On the basis of this latest data we have re-classified consumer debt as an unsatisfactory indicator at its present level. There is a portion of economic opinion that regards more debt as a positive driver of consumption as suggested by this extract from Economy.com: “Consumer credit is expected to climb in 2014, gaining traction as the economy improves. A healing labor market will boost income growth, supporting consumers’ balance sheets and giving them the confidence to borrow more to aid consumption. However, risks remain in the form of a falling stock market, high unemployment, and rising gas prices, which could undermine willingness to take on more debt.”

It seems to us that the “Great” recession did not flush out all the problems that built up over the last decade and that this is still a time to keep your business powder dry.