Market Data

February 7, 2014

The January 2014 Senior Loan Officer Opinion Survey on Bank Lending Practices

Written by Peter Wright

Once a quarter the Federal Reserve surveys the senior loan officers of domestic banks and U.S. branches and agencies of foreign banks. Questions cover changes in the standards and terms of the banks’ lending and the state of business and household demand for loans.

The January survey preamble was as follows: “The January 2014 Senior Loan Officer Opinion Survey on Bank Lending Practices addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months. Domestic banks, on balance, reported having eased their lending standards on many types of business and consumer loans and having experienced increases in loan demand, on average, over the past three months. The survey contained two sets of special questions. The first set asked about effects of the supervisory guidance on leveraged lending issued on March 21, 2013. The second set of questions asked banks about the outlook for loan performance for different categories of lending over 2014. This summary is based on the responses from 75 domestic banks and 21 U.S. branches and agencies of foreign banks.

“Regarding loans to businesses, the January survey results generally indicated that, on balance, banks eased their lending policies for commercial and industrial (C&I) loans to firms of all sizes and experienced stronger demand for such loans over the past three months. Almost all domestic banks that eased their C&I lending policies cited increased competition for such loans as an important reason for having done so. A modest fraction of foreign respondents indicated, on net, that they had eased standards on C&I loans, and a moderate net fraction of such banks reported that demand for C&I loans had increased somewhat. In response to the special questions on the supervisory guidance on leveraged lending, a number of large domestic and foreign banks indicated that they had tightened standards on such loans. Those banks also reported that some leveraged loans had been curtailed or significantly altered by the guidance, but a majority of them believed that affected borrowers would be able to turn to other sources of funding.

“On net, domestic institutions also reported having eased standards for most types of commercial real estate (CRE) loans and having experienced stronger demand for such loans. A modest net fraction of foreign respondents indicated that they had eased standards on CRE loans in the aggregate, while a large net fraction of such banks indicated that they had experienced stronger demand for such loans.

“Changes in standards and terms on, and demand for, loans to households were mixed. The survey results indicated that a modest fraction of large banks had eased standards on prime residential real estate loans, but a similar fraction of small banks had tightened standards on such loans. A moderate fraction of banks reported, on balance, weaker demand for prime mortgage loans to purchase homes, and a large net fraction reported weaker demand for nontraditional mortgage loans. Demand for home equity lines of credit (HELOCs) was little changed. Respondents indicated that they had eased standards on credit card loans, auto loans, and other consumer loans. Most banks reported little change in most terms on consumer loans, with the exception of credit card limits and loan rate spreads on auto loans, which modest fractions of banks reported having eased on balance. Modest net fractions of banks reported increases in demand for all types of consumer loans.

Survey respondents were asked about their expectations for loan delinquency and charge-off rates in 2014, assuming that economic activity progresses in line with consensus forecasts. Both domestic and foreign respondents generally indicated that they anticipated improvements in the performance of business loans. Domestic banks also reported that they expected improved performance for most types of loans to households, with the exception of auto loans to subprime borrowers, for which they expected increasing delinquency and charge-off rates in 2014.”

There is a huge amount of valuable data in this report which can be accessed here by those readers who wish to dig deeper.

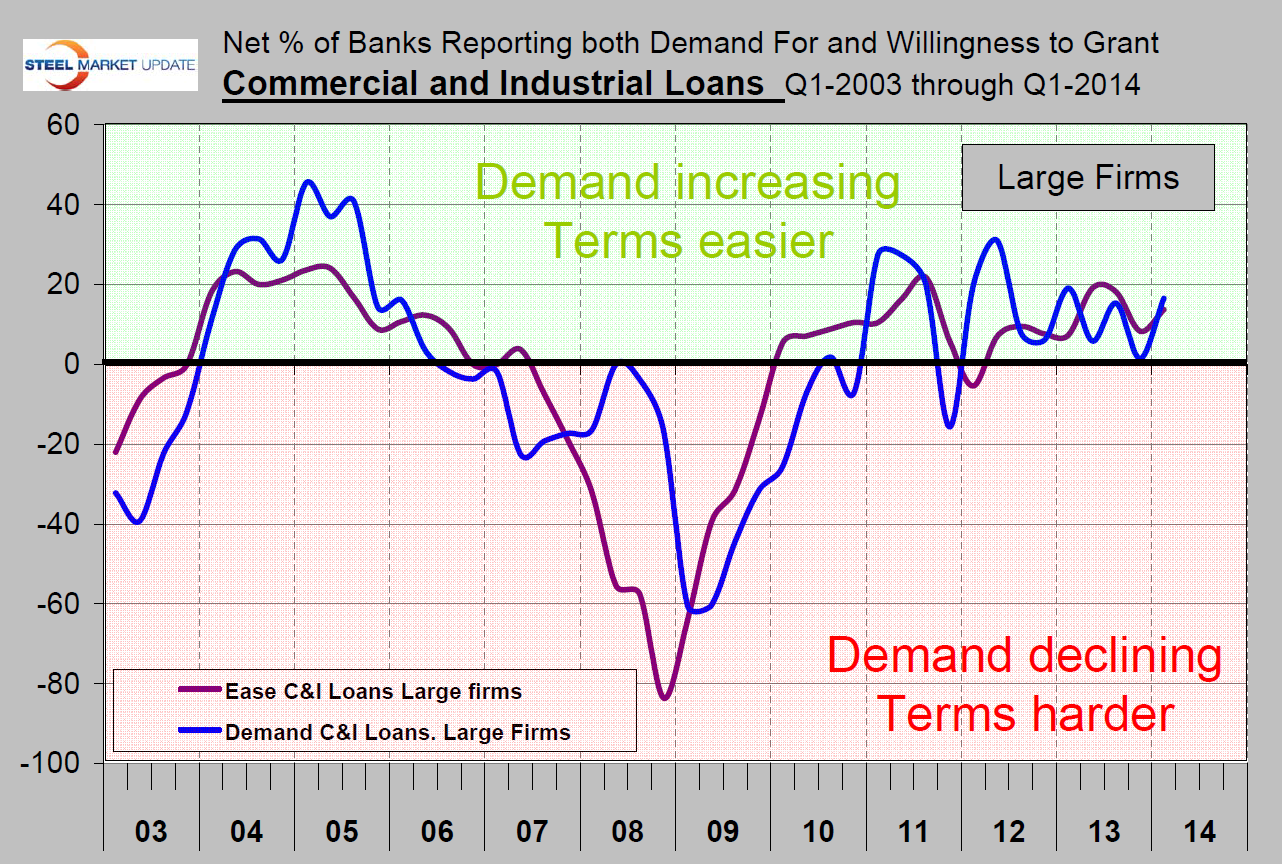

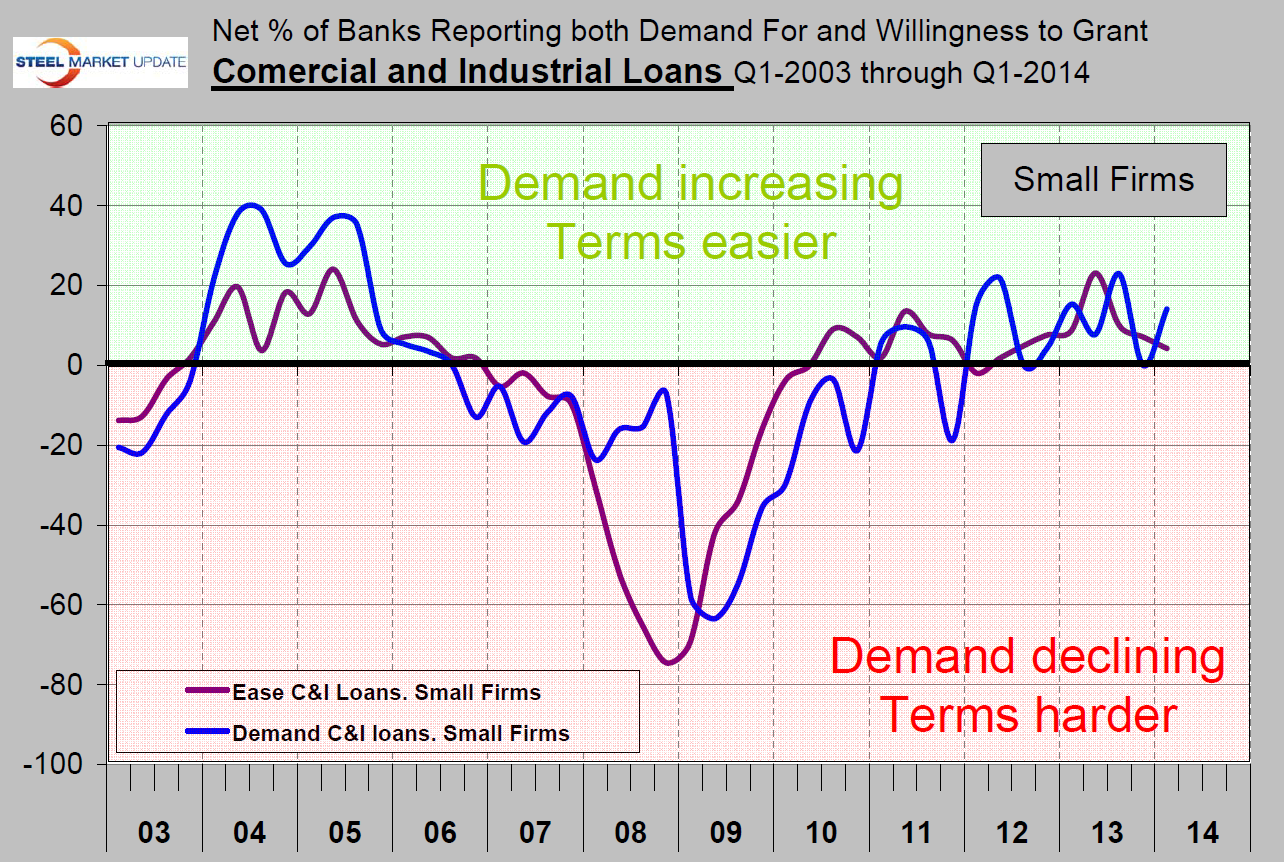

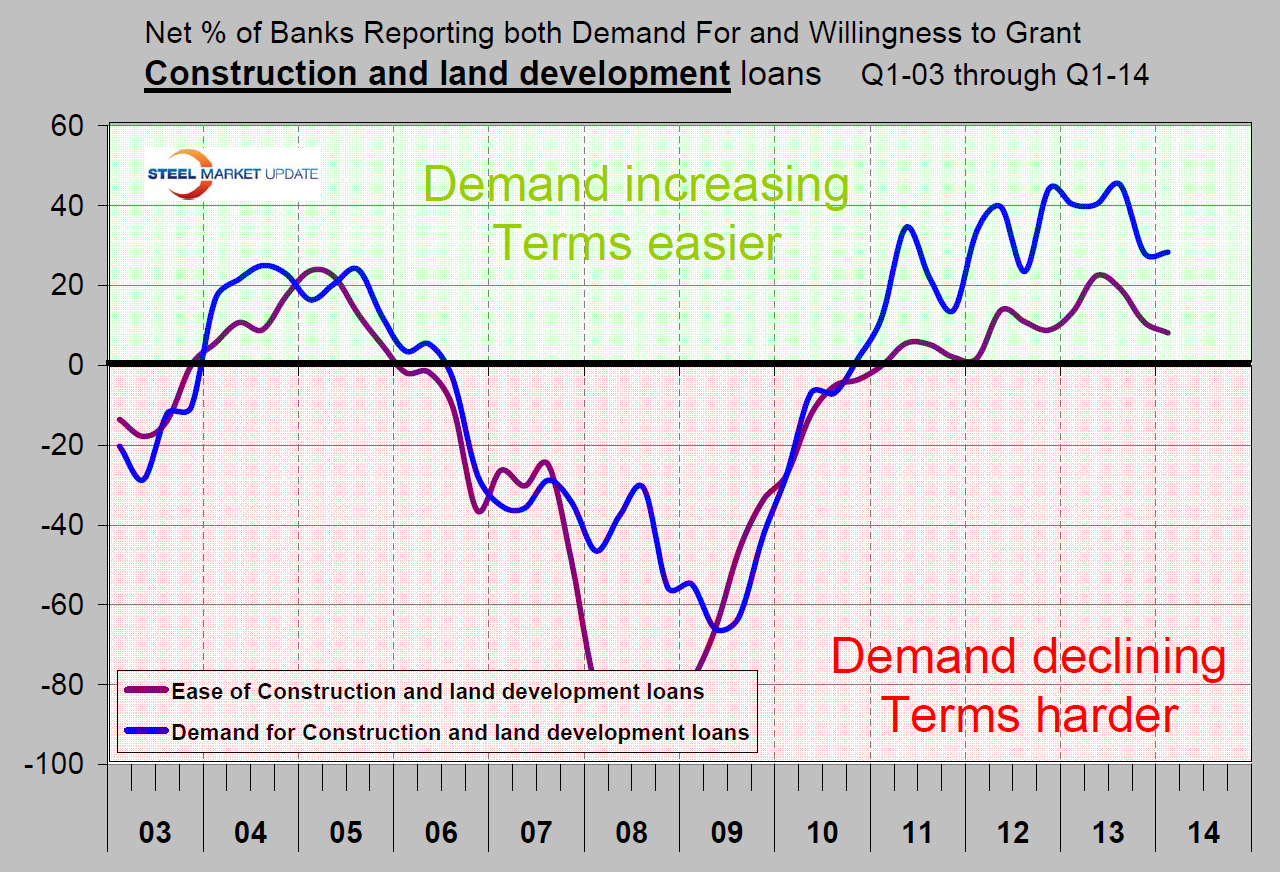

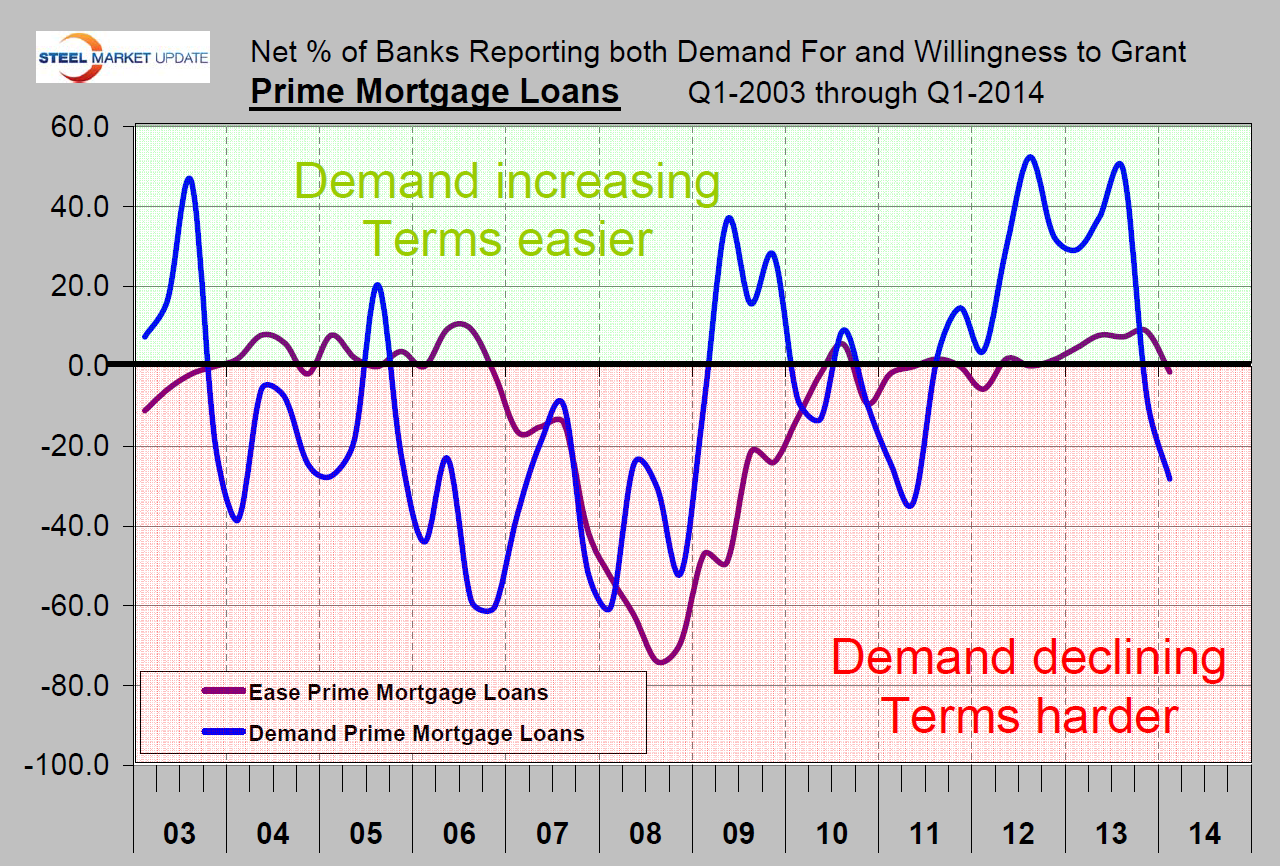

At SMU we extract and graph the major elements in the survey. Regarding loans to businesses, the January survey indicated that demand for commercial and industrial (C&I) loans from both large and small firms increased. Banks eased lending standards to large firms but the proportion of banks reporting an easing of terms to small firms decreased (Figures 1 and 2). A majority of banks are still reporting an increase in demand for and easier terms for construction and land development loans. Demand shot up in January to the point that a net 28.3 percent of banks were reporting an increase in demand (Figure 3). What this means is that the number of banks reporting an increase in demand was 28.3 percent higher than the proportion reporting a demand decrease. The bad news in this report is that a net 28.2 percent of banks reported a decrease in demand for prime mortgage loans and more banks were tightening standards than were loosening (Figure 4).

{kind=link}

{kind=link}

{kind=link}

{kind=link}