Product

February 13, 2013

SMU Price Ranges & Indices: Price Support Breaking Down

Written by John Packard

In one corner we have ArcelorMittal scratching and clawing and trying to hold on to at least a portion of their price increase. One week ago they were trying to collect $650. As the week progressed the number slipped a bit. This week…well, it slipped some more.

In the other corner we have a group of the other mills. As one buyer put it, “On a one by one basis all of them are willing to negotiate.” By how much will depend on the mill and the product.

SMU spoke to a non-automotive mill about their coating situation earlier this evening. We were told they were under pressure to not only sell at, but below, the prices they were at prior to the price increase announcements. However, their order book was stronger than it was then and they were not going to go below the old numbers. A sign of a bottom…at least for one mill.

Here is how we see spot prices this week:

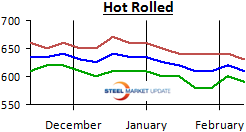

Hot Rolled Coil: SMU Range is $590-$630 per ton ($29.50/cwt-$31.50/cwt) with an average of $610 per ton ($30.50/cwt), fob mill, east of the Rockies. Both the lower and upper ends of our range declined by $10 per ton compared to where they were this time last week, resulting in our average declining $10 per ton. The trend for hot rolled remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Hot Rolled Coil: SMU Range is $590-$630 per ton ($29.50/cwt-$31.50/cwt) with an average of $610 per ton ($30.50/cwt), fob mill, east of the Rockies. Both the lower and upper ends of our range declined by $10 per ton compared to where they were this time last week, resulting in our average declining $10 per ton. The trend for hot rolled remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Hot Rolled Lead Times: 2-5 weeks.

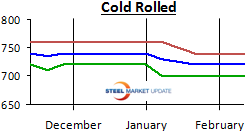

Cold Rolled Coil: SMU Price Range is $700-$740 per ton ($35.00/cwt-$37.00/cwt) with an average of $720 per ton ($36.00/cwt) fob mill, east of the Rockies. Both the lower and upper end of our range remained the same as one week ago. Our average also remained the same as it was one week earlier. The trend for cold rolled remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Cold Rolled Coil: SMU Price Range is $700-$740 per ton ($35.00/cwt-$37.00/cwt) with an average of $720 per ton ($36.00/cwt) fob mill, east of the Rockies. Both the lower and upper end of our range remained the same as one week ago. Our average also remained the same as it was one week earlier. The trend for cold rolled remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Cold Rolled Lead Times: 4-7 weeks.

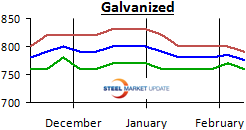

Galvanized Coil: SMU Base Price Range is $35.00/cwt-$36.50/cwt with an average of $35.75/cwt plus applicable extras, fob mill, east of the Rockies. The lower end of our range dropped by $10 per ton compared as did the upper end of our range. Our average is now $10 per ton less than one week ago. The trend for galvanized remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Galvanized Coil: SMU Base Price Range is $35.00/cwt-$36.50/cwt with an average of $35.75/cwt plus applicable extras, fob mill, east of the Rockies. The lower end of our range dropped by $10 per ton compared as did the upper end of our range. Our average is now $10 per ton less than one week ago. The trend for galvanized remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Galvanized .060” G90 Benchmark: SMU Range is $760-$790 per ton with an average of $775 per ton.

Galvanized Lead Times: 3-6 weeks.

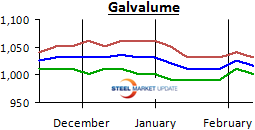

Galvalume Coil: SMU Base Price Range is $36.00/cwt-$37.00/cwt with an average of $36.50/cwt plus applicable extras, fob mill, east of the Rockies. The lower end of our range remained intact while the upper end of our range decreased by $10 per ton compared to one week ago. Our average also dropped by $5 per ton. The trend for Galvalume remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Galvalume Coil: SMU Base Price Range is $36.00/cwt-$37.00/cwt with an average of $36.50/cwt plus applicable extras, fob mill, east of the Rockies. The lower end of our range remained intact while the upper end of our range decreased by $10 per ton compared to one week ago. Our average also dropped by $5 per ton. The trend for Galvalume remains stuck in a “weak” neutral as prices drift based on the weekly needs of the domestic steel mills. At the moment, we do not see anything which will “push” prices firmly in one direction or another and we anticipate this drift to continue into early March.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $1011-$1031 per ton with an average of $1021 per ton.

Galvalume Lead Times: 5-8 weeks.