Product

January 7, 2013

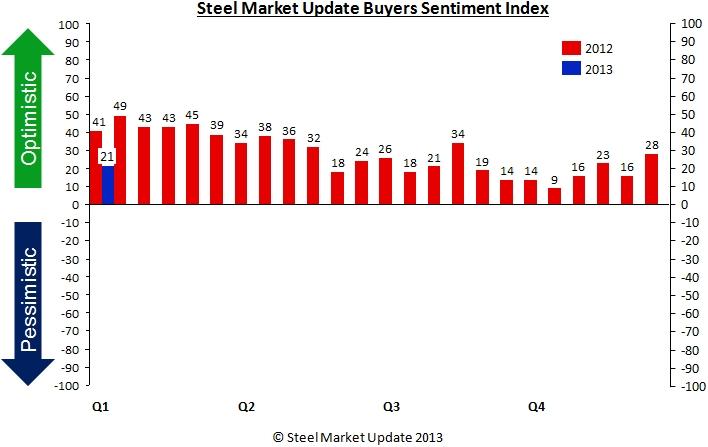

SMU Steel Buyers Sentiment Index Slightly Less Optimistic

Written by John Packard

After months of uncertainty related to governmental policies and the fiscal cliff negotiations (or lack thereof) combined with normal end of the year seasonal factors, steel buyers and sellers finished 2012 in the Optimistic range of the SMU Steel Buyers Sentiment index. During the first week of 2013 those same buyers and sellers were slightly less optimistic than they were during the middle of December as our SMU Steel Buyers Sentiment Index was measured at +21, down 7 points from the mid-Decemberwas measured at +21, down 7 points from the mid-December level. Compared to one year ago, Sentiment is 20 points lower than the +41 reported at this time last year.

Steel Market Update (SMU) invited 690 companies to participate in our survey, which began on Wednesday of this past week and ran through the end of the week. During the survey process a number of companies provided comments in order to explain the reasoning behind their responses.

A large Midwest-based service center told SMU, “Auto has been steady and looks like it will continue steady to slightly up. On the other hand, heavy truck and trailer is down and will probably stay that way through the first half of 2013.” This service center also reported demand as “declining.”

A trading company expressed frustrations held by many within the steel industry when they told us, “The only issue holding back a widespread and meaningful recovery is the inability of our elected officials to manage the country. It’s pathetic really. The fiscal cliff was averted, but is only the prelude to continued bickering and gridlock in resolving the foundational problems that remain.” This company reported demand as “improving” albeit at a “glacial pace.”

From a service center involved in the construction industry we heard, “No demand in the light gauge construction market.” For their company demand has been “remaining the same.”

A steel mill executive told us their order books were “healthy” and, “service center order books are good, autos are doing well and overall demand is stable to good.” In this mill’s eyes demand is “improving.”

While a construction-related manufacturing company reported, “Business continues to move upward in small ticks, we can’t complain.” For their company demand is “improving” but “only in small percentages.”

A service center executive told us, “December started slowly but picked up nicely so that we ended up exceeding forecast.” They told us demand, however, is “remaining the same.”

A HVAC wholesaler explained to SMU during the survey process, “HVAC in our area is a real concern, especially going into the first quarter as we are seeing business drop from a year ago.” They told us they are seeing demand as “declining.”

SMU Future Steel Buyers Sentiment Index

SMU Future Steel Buyers Sentiment Index was reported as slightly less optimistic having been measured at +45 down 2 points from mid-December levels and well below the +62 measured during the first week 2012. Even so, Future Sentiment is well within the optimistic range of our index.

SMU Future Steel Buyers Sentiment Index was reported as slightly less optimistic having been measured at +45 down 2 points from mid-December levels and well below the +62 measured during the first week 2012. Even so, Future Sentiment is well within the optimistic range of our index.

As with the current Sentiment Index, steel buyers and sellers reported having issues with uncertainty related to seasonal and governmental issues which pushed business out into the future. Here are a number of comments explaining the issues being faced by steel companies:

“Our back log into 2013 is favorable but most of the work will not start until 2nd Qtr. Election and fiscal cliff issues have held back may starts or decisions to start 1st Qtr jobs.” Manufacturing company.

“We feel it will more or less be a carbon copy of last year. Decent / steady demand and compressed margins.” Midwest Service Center.

“We employ price-risk methodologies and have flexibility in our supply contracts to minimize our exposure in times of uncertainty and instability.” National Service Center.

A manufacturing company responded their optimism was based on their ability to increase market share, “New business will drive this, not increased demand from existing customers.”

About the SMU Steel Buyers Sentiment Index

SMU Steel Buyers Sentiment Index is a measurement of the current attitude of buyers and sellers of flat rolled steel products in North America regarding how they feel about their company’s opportunity for success in today’s market. It is a proprietary product developed by Steel Market Update for the North American steel industry.

Positive readings will run from + 10 to + 100 and the arrow will point to the right hand side of the meter located on the Home Page of our website indicating a positive or optimistic sentiment.

Negative readings will run from -10 to -100 and the arrow will point to the left hand side of the meter on our website indicating negative or pessimistic sentiment.

A reading of “0” (+/- 10) indicates a neutral sentiment (or slightly optimistic or pessimistic) which is most likely an indicator of a shift occurring in the marketplace.

Readings are developed through Steel Market Update market surveys which are conducted twice per month. We display the index reading on a meter on the Home Page of our website for all to enjoy.

Currently we send invitations to slightly less than 700 North American companies to participate in our survey. Our normal response rate is approximately 130-200 companies. Of those responding to this week’s survey 44 percent were manufacturing companies, 40 percent were service centers/distributors and the balance was made up of steel mills, trading companies and toll processors involved in the steel business.

Steel Market Update does canvass those being invited to participate in order to confirm their active participation in the flat rolled steel business. Our list is updated at least once per month and we are adding new companies on a continuous basis.